What credit score is needed to buy a house?

Your credit scores can be an important factor in the home-buying process. That’s because the lender will typically check your credit scores when you apply for a mortgage.

A good credit score generally makes you an attractive borrower because it shows you’ve managed your credit well. And the better your credit scores, the better chance you may have of being approved for a mortgage—and at a lower interest rate.

The minimum credit score needed to buy a house depends on the mortgage program and the lender. According to mortgage company Fannie Mae, a conventional loan usually requires a credit score of at least 620. But you may qualify for a government-sponsored loan with a lower score. Read on to learn more about credit scores and how they impact the home-buying process.

Key takeaways

- Borrowers applying for conventional mortgage loans might need a credit score of 620 or higher to qualify.

- Requirements for government-backed loans—like FHA loans, VA loans and USDA loans—change depending on the size of down payments, the lender and more.

- Making on-time payments, keeping your credit utilization low and avoiding unnecessary credit applications can help improve your credit scores before buying a house.

Minimum credit score to buy a house by loan type

When applying for common mortgage types like conventional loans or government-backed loans—like FHA loans, VA loans and USDA loans—you can typically expect lenders to require the following minimum credit scores:

| Mortgage loan type | Minimum credit score requirement |

|---|---|

| Conventional loan | 620 |

| FHA loan | 500 with a 10% down payment, 580 with a 3.5% down payment |

| VA loan | No minimum score |

| USDA loan | 640 for direct USDA loans, 680 for guaranteed USDA loans |

Conventional loans

A conventional loan is a mortgage that’s not insured by a government agency. Most conventional loans are backed by mortgage companies Fannie Mae and Freddie Mac.

Fannie Mae says that conventional loans typically require a minimum credit score of 620. But lenders can raise their own requirements.

Keep in mind: For a conventional mortgage, you’ll also typically need a low debt-to-income ratio, which measures how much of your monthly income goes toward debt expenses. Lenders usually look for a debt-to-income ratio of 43% or less, according to the Consumer Financial Protection Bureau (CFPB).

FHA loans

Mortgages insured by the Federal Housing Administration (FHA) are designed for people with less-than-perfect credit. These loans require smaller down payments than other types of mortgages.

The U.S. Department of Housing and Urban Development (HUD) says you may qualify for an FHA loan with a credit score of 500 as long as you put down at least 10%. With a higher credit score—one that’s at least 580—you may qualify with a down payment as low as 3.5%.

VA loans

VA loans are loans that are guaranteed by the U.S. Department of Veterans Affairs. They’re meant for veterans, active-duty military members and eligible surviving spouses. The VA doesn’t set a minimum credit score for these home loans, and lenders can develop their own requirements.

USDA loans

USDA loans are backed by the U.S. Department of Agriculture and are for homes in eligible rural areas. There are two main types of USDA mortgages. Direct loans are funded by the USDA, while guaranteed loans are funded by private banks and insured by the USDA.

The USDA has flexible eligibility requirements for these loans. According to the USDA, borrowers typically need a credit score of at least 640 for the direct loan and at least 680 to qualify for the guaranteed loan.

What is a good credit score for buying a house?

A credit score that’s considered “good” or better may help you qualify for lower mortgage interest rates, according to the CFPB. And lower interest rates can help keep your borrowing costs low. The CFPB says people with credit scores in the mid-700s or beyond qualify for the best mortgage rates.

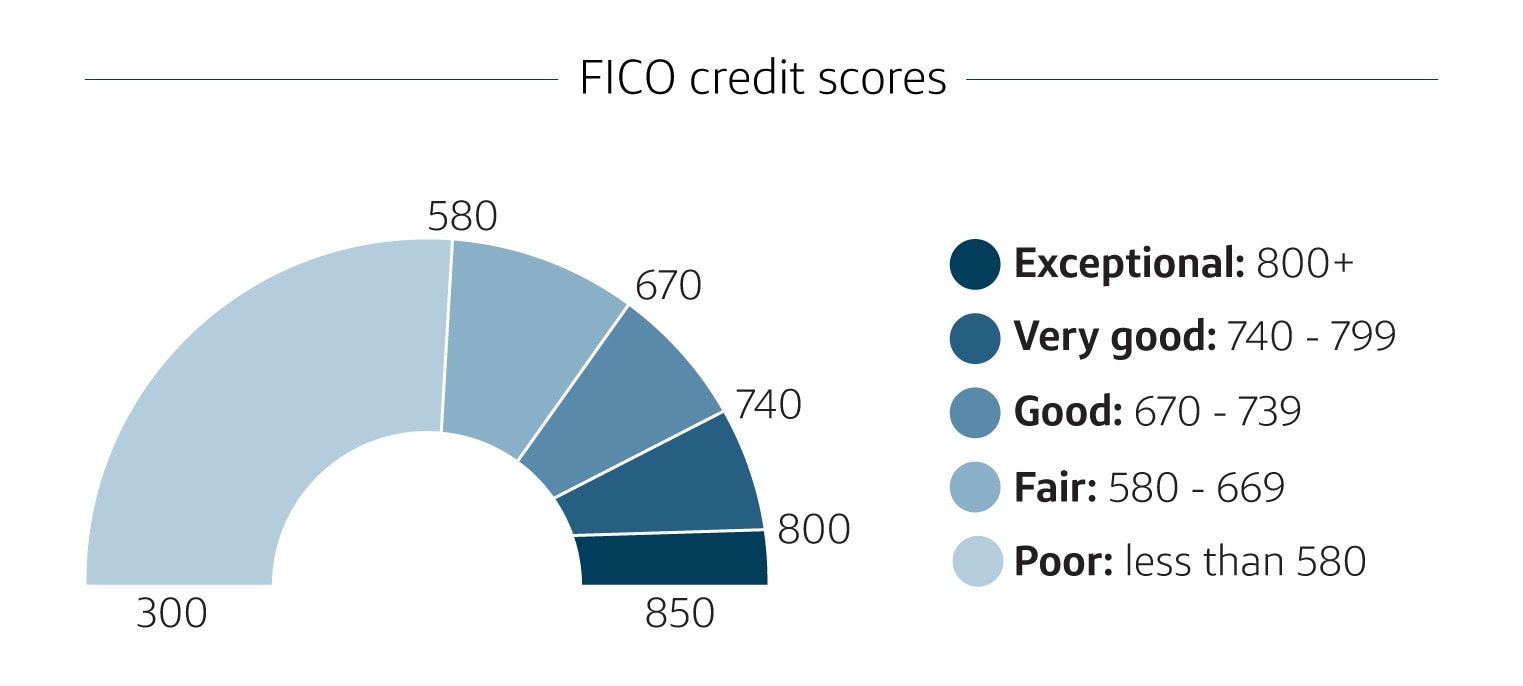

Lenders tend to look at credit scores in ranges. And, as the CFPB notes, lenders award the best interest rates to people with the highest credit scores. For example, here’s how FICO® groups credit scores and how those scores might impact the rate you get:

Source: MyFICO.com

- Exceptional (800–850): People with exceptional credit scores have generally shown they pay back money as agreed and may qualify for the best interest rates.

- Very good (740–799): This credit score range is considered above average. As a very dependable borrower, you’re likely to qualify for attractive loan terms.

- Good (670–739): A credit score within this range can help you qualify for a loan, though interest rates may start climbing compared with someone with a higher credit score.

- Fair (580–669): Although these borrowers have a below-average credit score, lenders typically still approve them for mortgage loans.

- Poor (350–579): A poor credit score shows you’re a risky borrower, which may make it harder to qualify for a mortgage. Those who are eligible will likely pay higher interest rates.

Keep in mind that there are multiple credit scores and scoring models. And scoring companies like FICO and VantageScore® have different versions of their own scores. So you might see slight differences in your scores depending on what model was used.

How can credit scores affect mortgage interest rates?

The CFPB points out that your credit scores are a key ingredient in the mortgage qualification process and that higher credit scores generally help you qualify for lower interest rates. To see the potential impact of credit scores on mortgage interest rates, it helps to look at the following example:

Let’s say two borrowers apply for a 30-year fixed mortgage for $200,000. Borrower A has a credit score in the 620 to 639 range, while Borrower B has a score between 760 and 850. According to FICO’s home mortgage rate comparison tool, the borrowers’ potential mortgage rates could differ by about 1.5%.

While that may not sound like much, according to the results of that tool, the borrower with the lower credit score—Borrower A—pays $173 more every month. And that extra $173 every month adds up over time.

Ways to help strengthen credit scores before buying a house

If your credit scores need work before you buy a house, consider these ways to help improve your scores:

- Make on-time payments. FICO and VantageScore both say your track record of making on-time payments on outstanding debts—your payment history—can be a significant factor in determining your credit rating. To build more consistent repayment habits, you could use email reminders or calendar alerts to remind yourself of upcoming bills. And setting up automatic payments can help ensure you don’t miss a payment due date.

- Keep your balances low. The CFPB recommends that you not spend more than 30% of your available credit. A low credit utilization ratio—a measure of how much of your available credit you’re using—could be a sign that you’re using your credit responsibly and not overspending. And that could help you improve your score.

- Pay more than the minimum. Making only your credit card minimum payments comes with a cost: interest charges. And interest can add up and cost you more money in the long run. Interest can even make it harder to pay off debt. So consider this from the CFPB: “Paying off your balance each month can help you get the best scores.”

- Apply only for the credit you need. As the CFPB explains, “Credit scoring formulas look at your recent credit activity as a signal of your need for credit. If you apply for a lot of credit over a short period, it may appear to lenders that your economic circumstances have changed negatively.”

If your credit scores are still too low to get approved for a mortgage, it might also be worth considering asking if having a co-signer is an option. Even with a co-signer, it’s worth considering how your monthly mortgage payment fits into your budget.

In a nutshell: Credit scores needed to buy a house

It’s generally a good idea to check your credit and see where you stand before you apply for a mortgage.

With CreditWise from Capital One, you can access your free credit report and credit score anytime—even if you’re not a Capital One account holder.

You can also get free credit reports from each of the three major credit bureaus. Visit AnnualCreditReport.com to learn how.

Looking for more tips on how to boost your credit before buying a house? Check out this guide on seven ways to improve your credit scores.