VantageScore® vs. FICO®: Different types of credit scores

You might already know there are different types of credit scores—and that you may have more than one. That’s because there are multiple credit-scoring companies. And they each have multiple scoring models that can be used to calculate credit scores.

Keep reading to learn more about two of those credit-scoring companies, VantageScore and FICO.

What you’ll learn:

-

Credit scores are based on the information in credit reports and are used to make lending decisions.

-

VantageScore and FICO are the credit-scoring companies most commonly used by lenders.

-

Credit-scoring companies each have their own credit-scoring models for determining credit scores.

- Consumers often have multiple credit scores, because there are multiple credit-scoring companies and models.

Credit scores: What you need to know

Think of your credit scores like a snapshot of your credit reports, which contain information about your credit history and habits. This includes things like your payment history, account balances and types of credit accounts, such as credit cards, personal loans and student loans.

Credit-scoring companies like VantageScore and FICO calculate credit scores by applying the information in credit reports to mathematical formulas called scoring models.

VantageScore vs. FICO: Similarities and differences

There are multiple credit bureaus, credit-scoring companies and credit-scoring models. So your credit scores can change depending on what information is used to calculate it, what company calculates it and when it’s calculated. That’s why it’s normal to have more than one credit score.

And scoring models might use information from just one credit report—or a combination of different reports. Then each credit-scoring formula might assign different levels of importance to that information.

In other words, there are a lot of variables that make each credit-scoring company and model a bit different.

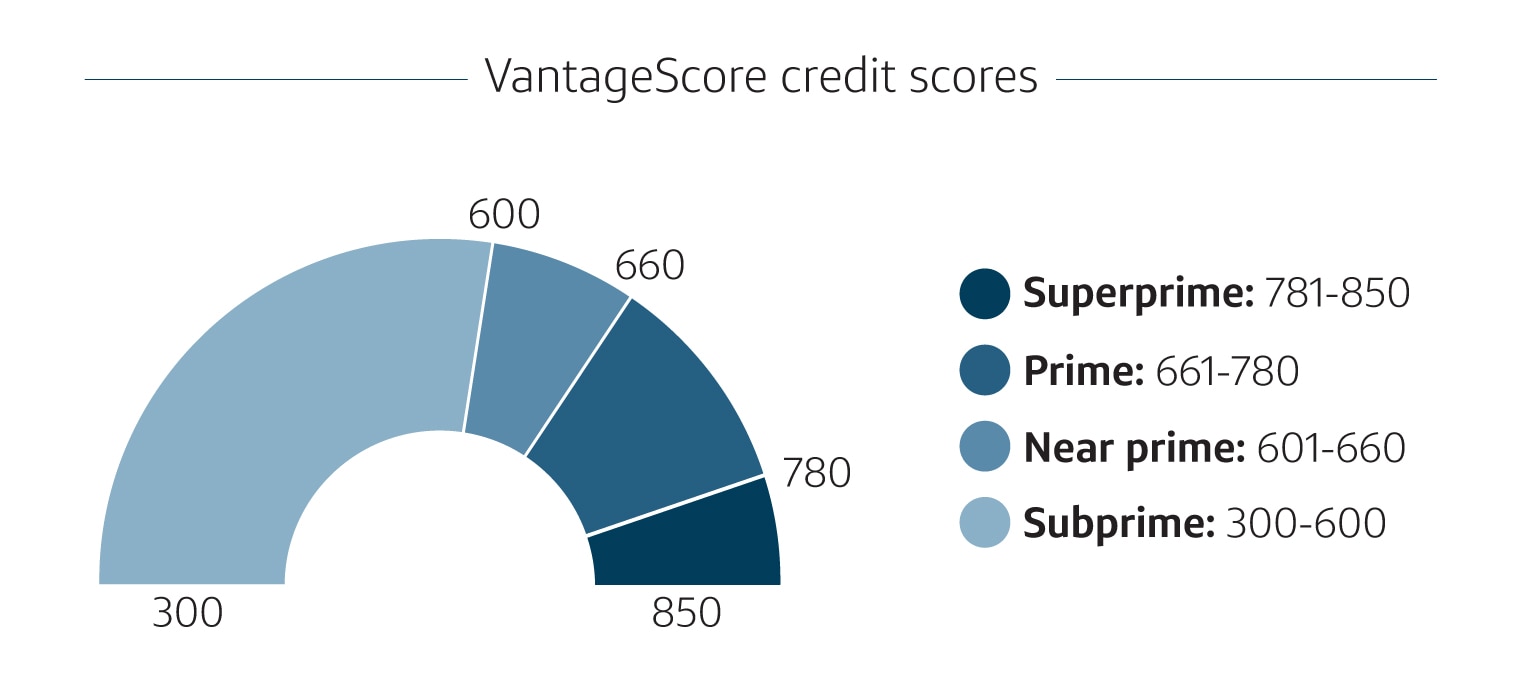

What is a VantageScore credit score?

VantageScore uses various credit-scoring models, and their latest scores range from 300 to 850. Different factors go into a VantageScore credit score. For example, the VantageScore 4.0 model is weighted like this:

-

Payment history: 41%

-

Depth of credit, which includes factors like credit mix and age of accounts: 20%

-

Credit utilization: 20%

-

Recent credit: 11%

-

Balances: 6%

-

Available credit: 2%

VantageScore says prime credit scores that fall between 661 and 780 are considered good. Here’s how it categorizes the rest of its scores:

-

Superprime: 781-850

-

Prime: 661-780

-

Near prime: 601-660

- Subprime: 300-600

Source: VantageScore.com

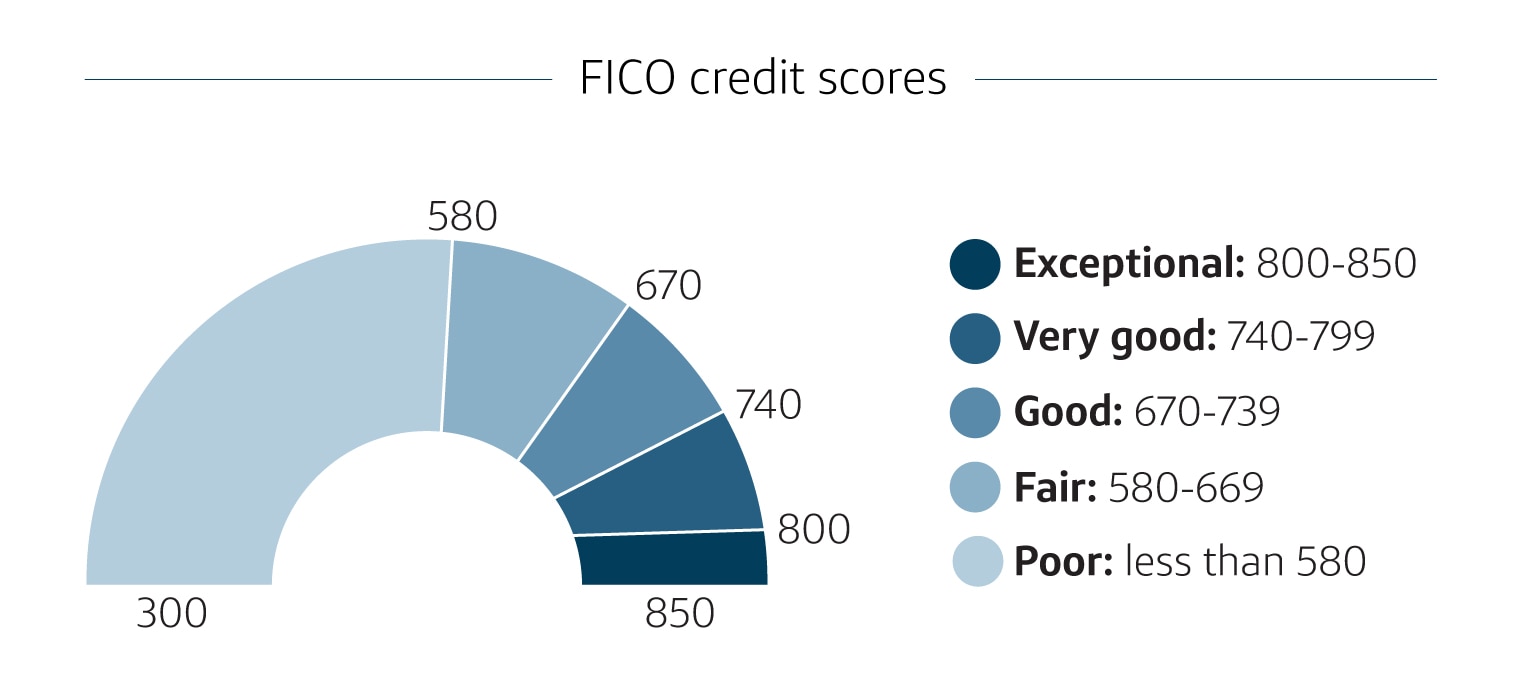

What is a FICO score?

According to FICO, its scores are the most widely used by lenders. FICO credit scores generally range from 300 to 850. FICO also has industry-specific scoring models. That includes FICO Auto Score and FICO Bankcard Score. These industry-specific scores range from 250 to 900.

But for general scores, such as FICO 8, the company considers specific categories when calculating credit scores:

-

Payment history: 35%

-

Total debt: 30%

-

Length of credit history: 15%

-

Credit mix: 10%

-

New credit: 10%

If you’re trying to determine where your score falls, FICO provides the following ranges:

-

Exceptional: 800+

-

Very good: 740-799

-

Good: 670-739

-

Fair: 580-669

- Poor: Less than 580

Source: My FICO.com

VantageScore vs. FICO: At a glance

Even if their descriptions differ, the criteria VantageScore and FICO use to calculate credit scores are pretty similar. Here’s a general look at how they compare:

|

VantageScore score categories |

VantageScore ranges |

FICO score categories |

FICO ranges |

|

Superprime |

781-850 |

Exceptional |

800+ |

|

Prime |

661-780 |

Very good |

740-799 |

|

Near prime |

601-660 |

Good |

670-739 |

|

Subprime |

300-600 |

Fair |

580-669 |

|

Poor |

Less than 580 |

VantageScore vs. FICO FAQ

If you feel like you’ve gotten the basics down, it might be time to dive a little deeper with these frequently asked questions.

Is VantageScore accurate?

VantageScore’s credit scores are based on credit reports from the three major credit reporting agencies: Equifax®, Experian® and TransUnion®. If they’re calculated using accurate information, VantageScore credit scores are just as accurate as any other credit score.

Ultimately, decisions about loan and credit applications are made by lenders.

Why is my VantageScore higher than my FICO scores?

VantageScore’s credit scores aren’t necessarily higher than FICO’s scores. VantageScore and FICO scores may differ, because they use different scoring models.

Scores are also dependent on the information used to calculate them and when they’re calculated.

Do banks use FICO or VantageScore?

Both FICO and VantageScore credit scores can be used by lenders and credit card issuers when evaluating creditworthiness. But whether a VantageScore or FICO score is used depends on the lender.

Key takeaways: VantageScore vs. FICO score

With different scoring models and credit-scoring companies, having different credit scores is normal. Understanding how your credit scores are calculated could help you better understand how to build good credit and improve your odds of being approved for a loan or a credit card.

One way to monitor your credit is with CreditWise from Capital One. CreditWise gives you access to your credit report and credit score—without hurting your scores. And CreditWise is available to everyone—even if you don’t have a Capital One account. You can also get free copies of your credit reports from each of the major credit bureaus at AnnualCreditReport.com.