What is a credit score?: A beginner’s guide

Credit scores are essentially snapshots of a person’s credit history. And they can affect everything from lending decisions and loan terms to rental applications and insurance premiums.

But how are credit scores calculated? What qualifies as a good credit score? And how can you build and maintain good credit scores? Read on to learn more.

Key takeaways

-

Credit scores reflect a person’s creditworthiness and how likely they are to pay back their debts on time.

-

Credit scores are used in lending decisions and can affect other things too.

-

Credit reports are used by credit-scoring companies to calculate credit scores.

-

The higher the credit score, the better.

What is a credit score, and how is it used?

A credit score is a three-digit number used to predict how likely a person is to pay their debts on time. Credit scores are a reflection of a person’s creditworthiness and indicate how healthy their credit is.

A person’s scores are based on their credit history, which is compiled into credit reports by credit bureaus—also known as credit reporting agencies—like Equifax®, Experian® and TransUnion®.

How is a credit score calculated?

Credit scores are calculated based on the different factors in your credit reports. These factors are:

-

Payment history: How well you’ve done with making payments on time

-

Debt: How much unpaid debt you currently have across all of your accounts

-

Credit age: How long you’ve had your accounts open

-

Credit mix: The different types of credit accounts you have

-

New credit applications: How many times you’ve recently applied for credit

How exactly these factors affect your scores depends on the credit-scoring model—a mathematical formula used by a credit bureau—and the company doing the scoring. A model might use information from a combination of different credit reports or just one report. Then, each credit-scoring model might assign different levels of importance to that information.

FICO® and VantageScore® are the two credit-scoring companies that provide some of the most commonly used scores. But keep in mind that you have many different credit scores that different lenders use. And as the Consumer Financial Protection Bureau (CFPB) explains, “your score can differ depending on which credit reporting agency provided the information, the scoring model, the type of loan product and even the day when it was calculated.”

What is a good credit score to have?

What’s considered a good credit score depends on a variety of factors—like where the score comes from, who calculates it and who’s judging it.

But generally speaking, the higher the credit score, the better.

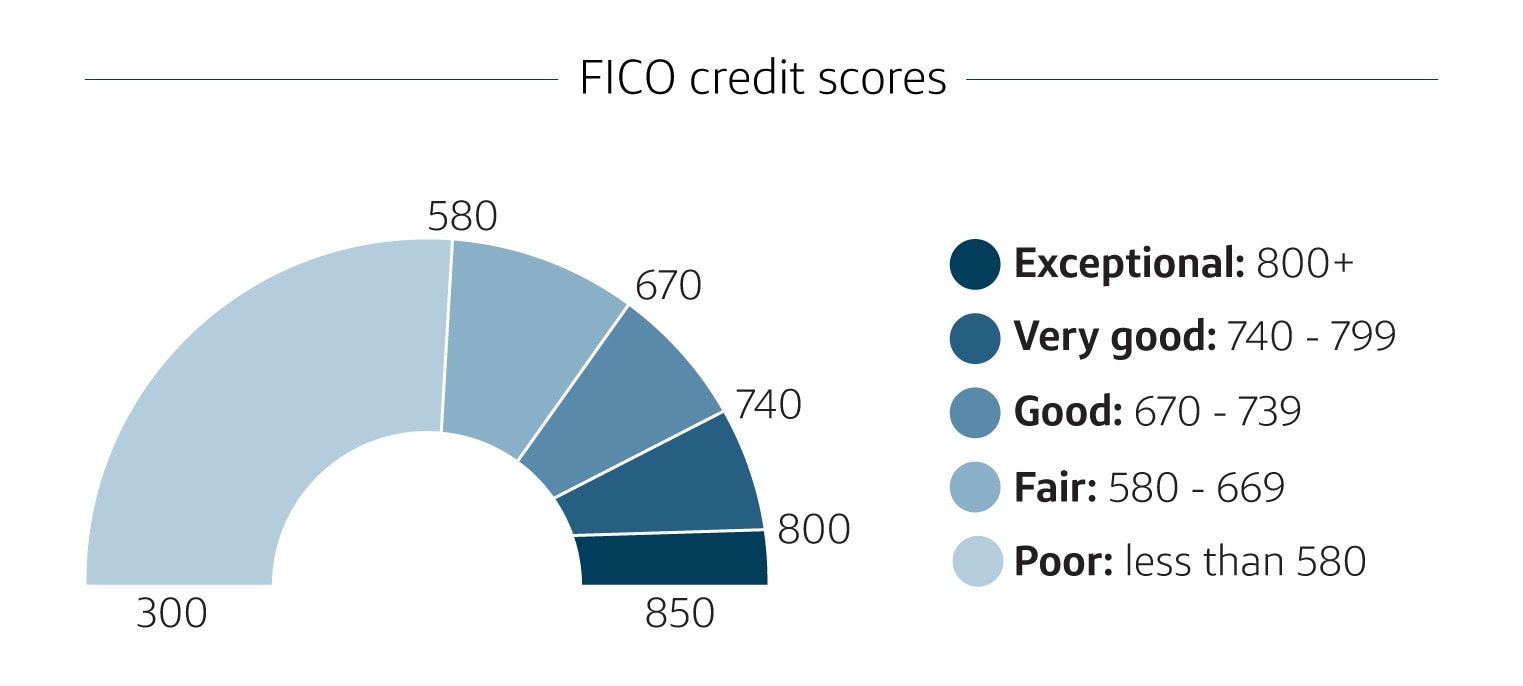

Good FICO credit scores

FICO scores that range between 670 and 739 qualify as good scores. Here’s a breakdown of how FICO categorizes their credit scores:

-

Exceptional: 800+

-

Very good: 740-799

-

Good: 670-739

-

Fair: 580-669

-

Poor: Less than 580

Source: MyFICO.com.

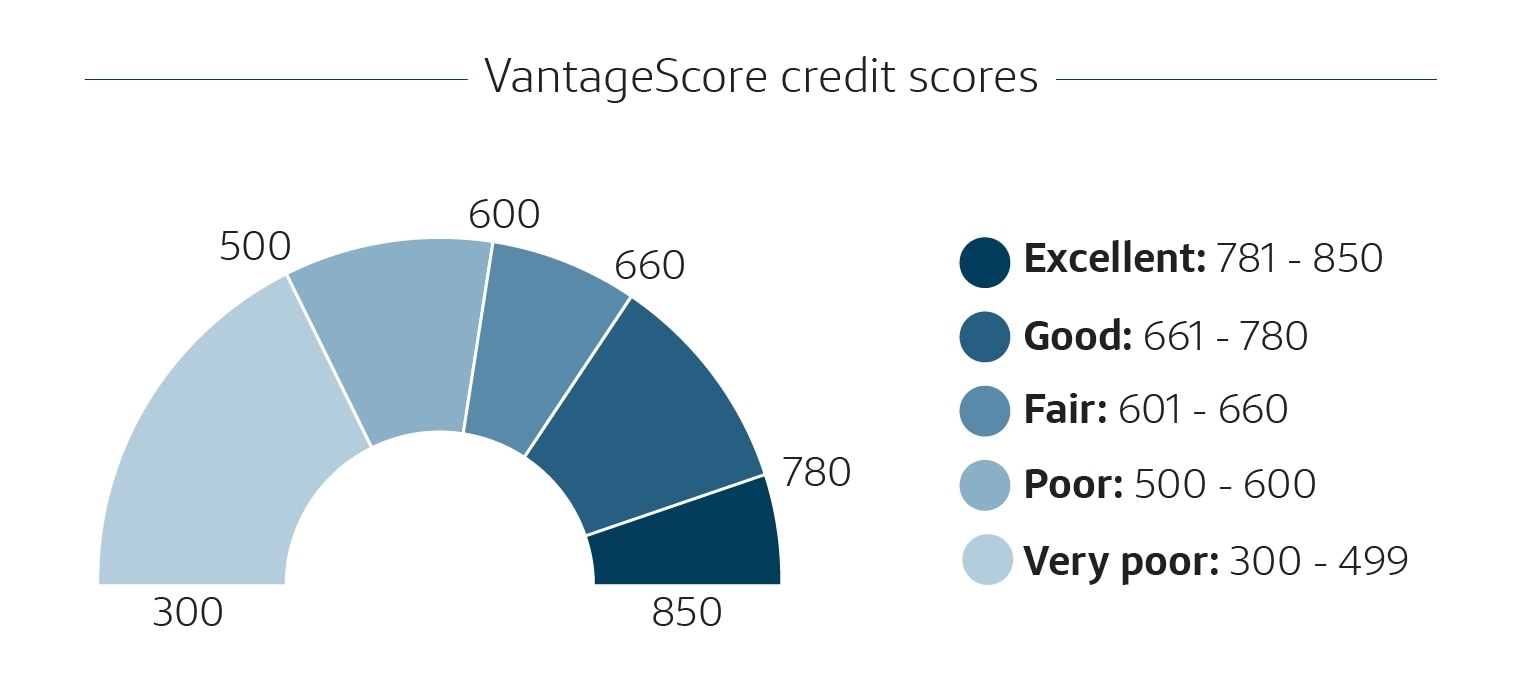

Good VantageScore credit scores

VantageScore considers good scores to be those between 661 and 780. Here’s how VantageScore defines different credit score ranges:

-

Excellent: 781-850

-

Good: 661-780

-

Fair: 601-660

-

Poor: 500-600

-

Very poor: 300-499

Source: VantageScore.com.

Why is a good credit score important?

Credit scores often come into play in lending decisions. Individuals with better credit scores often have an advantage when it comes to credit terms. When someone applies for credit, for example, their credit scores can affect credit limits and interest rates. They can even affect other things too:

-

Landlords may check credit scores as part of rental applications.

-

Insurers may consider credit to determine premiums.

-

Cellphone and utility providers may waive security deposits if they see good credit scores.

How do I build my credit score?

Building a good credit score and maintaining a good credit score come down to using credit responsibly over time.

According to the CFPB, here are a few keys to using credit responsibly:

-

Always pay your bills on time.

-

Stay well below your credit limits. Experts recommend keeping your credit utilization below 30% of your available credit across all your credit card accounts.

-

Apply only for the credit you need. If you apply for multiple credit cards and loans over a short period of time, lenders may think your financial situation has changed for the worse.

It’s also important to regularly monitor your credit so you can see where you stand and keep an eye on the factors that impact your credit scores.

You can get free copies of your credit reports at AnnualCreditReport.com. And with CreditWise from Capital One, you can access your credit scores anytime—without negatively impacting your score.

Credit score FAQ

Learn more about credit scores with these frequently asked questions:

Who calculates credit scores?

Several different sources, like credit reporting agencies, lenders and mortgage companies, may all calculate different types of credit scores.

Where can I get my credit scores?

In addition to requesting your credit scores from the three major credit bureaus, you can access your credit scores with CreditWise. You may also be able to find your credit score on your monthly credit card statement or via your credit card company’s website or app.

What’s a good credit score for my age?

In general, a credit score of 700 or above is considered good for all ages. And most consumers have credit scores that range from 600 to 750. But keep in mind that your age doesn’t factor into determining your credit score—neither do demographics like race and marital status.

Credit scores in a nutshell

Credit scores are a reflection of a person’s credit reports and credit history. Scores are used to predict how likely someone is to pay their debts on time. And they can affect lending decisions and loan terms as well as things like rental applications and insurance premiums.

Generally speaking, the higher the credit score, the better. And you can start building a higher credit score—and establishing good credit habits—by making payments on time, keeping balances well below your credit limits and only applying for credit you really need. Monitoring your credit scores and reports can also help you keep tabs on your progress and identify any errors that could negatively impact your credit scores.