What affects your credit scores?

You might know that credit-scoring companies use the information from your credit reports to calculate your credit scores. But what kinds of information are your scores based on? And how does that information impact your scores?

Read on to learn about what does and doesn’t impact your credit scores.

Key takeaways

- Companies such as FICO® and VantageScore® calculate credit scores.

- Credit scores are calculated using complex mathematical formulas called scoring models.

- As part of their calculations, scoring models take different factors into account to determine a credit score. Those factors include payment history, current debt, credit age, credit mix and recent credit applications.

- There are a number of ways to monitor credit scores, including free tools like CreditWise from Capital One.

5 factors that affect your credit scores

There are a few factors that affect your credit scores:

- Payment history

- Debt

- Credit age

- Credit mix

- New credit applications

How they affect your scores depends on the credit-scoring model and the company doing the scoring.

As the Consumer Financial Protection Bureau (CFPB) explains, FICO and VantageScore are the two credit-scoring companies that provide some of the most commonly used scores. So let’s take a look at each of the different factors and how they can affect your scores from FICO and VantageScore.

Payment history

Payment history is a key part of your credit history. It shows how well you’ve done with making payments on time.

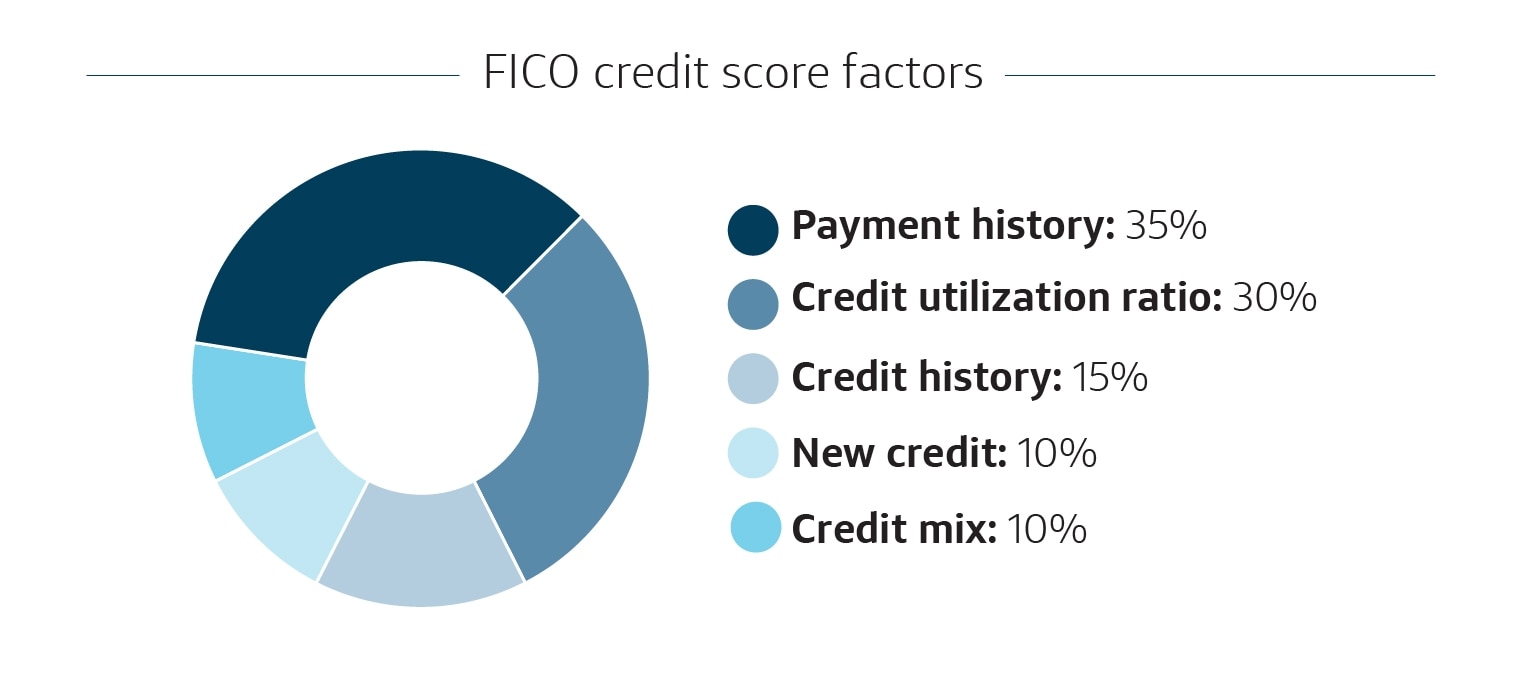

Both FICO and VantageScore put a lot of weight on payment history when calculating your credit scores. In fact, it’s the primary scoring factor at FICO and accounts for 35% of that score.

Why does payment history get so much attention? Because it can be a strong indicator of how you might handle future payments. And falling behind on payments could lead to negative information on your credit report—which includes things like late credit card payments and charge-offs—and adversely impact your credit.

Debt

Credit-scoring models consider how much unpaid debt you currently have across all your accounts. And they pay close attention to your credit utilization ratio—a ratio that reflects how much of your available credit you’re using.

Your credit utilization ratio is typically expressed as a percentage. According to the CFPB, experts recommend keeping your credit utilization below 30% of your total available credit. That’s because a low credit utilization ratio could be a sign that you’re using your credit responsibly and not overspending.

Credit age

Your credit age shows how long you’ve had your accounts open. “A longer credit history will always have a positive effect on FICO scores,” according to FICO.

That’s because, as the CFPB explains, “Credit scores are based on experience over time. The more experience your credit report shows with paying your loans on time, the more information there is to determine whether you are a good credit recipient.”

Credit mix

Your credit mix is made up of the different types of credit accounts you have. It takes into account both your revolving credit—like credit cards, personal lines of credit and home equity lines of credit—and your installment loans. Auto loans, mortgages, student loans and personal loans are all examples of installment loans.

Your credit mix is important because it shows how much experience you have with handling different types of credit. But keep in mind that a diverse credit mix won’t help your credit scores if you don’t use your credit responsibly.

New credit applications

This factor takes into account how many times you’ve recently applied for credit. The effect on your scores might be minor, but a lot of new hard credit inquiries could still give a negative impression to lenders.

“Credit scoring formulas look at your recent credit activity as a signal of your need for credit. If you apply for a lot of credit over a short period of time, it may appear to lenders that your economic circumstances have changed negatively,” says the CFPB.

What factor has the biggest impact on your credit scores?

Credit-scoring companies weigh factors differently. You can learn more about the differences between VantageScore and FICO. But just know there are a lot of variables, according to the CFPB.

“Each credit score depends on the data used to calculate it, and it may differ depending on the scoring model … the source of the data used, and even the day when it was calculated,” the agency says.

How FICO views credit score factors

FICO is clear about how it weighs credit-scoring factors, with payment history carrying the most weight, followed by amounts owed, credit age, credit mix and new applications.

How VantageScore views credit score factors

While VantageScore doesn’t give percentages, it’s clear about what’s crucial to its scoring. VantageScore says your unpaid debt is extremely influential. Credit mix is highly influential. Payment history is moderately influential. And credit age and new credit are less influential.

Factors that don’t affect your credit scores

While many factors affect your credit scores, some have no effect at all. In some cases, using them as a basis for lending decisions is even illegal.

- Your color, race, religion and sex

- Your marital status

- Where you’re from and where you live

- Credit checks by employers

- Checking your own credit reports and credit scores

How to monitor your credit for changes

It’s important to regularly monitor your credit if you’re trying to maintain or improve your credit scores. Monitoring your credit can help you see exactly where you stand—and how much progress you’ve made.

One way to monitor your credit is with CreditWise. CreditWise gives you free access to your credit report and credit score anytime. And using it won’t hurt your credit scores. You can even explore the potential impact of your financial decisions before you make them with the CreditWise Credit Score Simulator.

CreditWise is free and available to everyone—even if you’re not a Capital One account holder.

You can also get free copies of your credit reports from all three major credit bureaus—Equifax®, Experian® and TransUnion. Call 877-322-8228 or visit AnnualCreditReport.com to learn more.

FAQ about what affects your credit

Does paying bills affect your credit scores?

The answer depends on the type of bill, whether your payments are reported to the credit bureaus and how the scoring model considers that information. Learn more with this guide on why paying bills might help build credit.

Does having a credit application denied hurt your credit scores?

Getting denied for a credit card doesn’t affect your credit scores directly. However, applying for credit may lower your credit scores—usually by just a few points, according to FICO—because it may trigger a hard inquiry. That’s why the CFPB recommends applying only for the credit you need.

Want a better idea of whether you might be approved before you trigger a hard inquiry? Pre-approval or pre-qualification can help you find out whether you might be eligible for a credit card or loan before you even apply.

With Capital One’s pre-approval tool, for example, you can find out whether you’re pre-approved for some of Capital One’s credit cards before you submit an application. It’s quick and only requires some basic information. And checking to see whether you’re pre-approved won’t impact your credit scores.

What hurts your credit scores?

Here are a few factors that can cause a drop in your credit scores:

- Missing payments

- Having a short credit history

- Using too much of your total available credit

- Having accounts in collections

- Defaulting on accounts

Credit score factors in a nutshell

There are different factors that can affect credit scores. And their overall impact can vary depending on the credit-scoring company. Monitoring your credit with a tool like CreditWise can give you a better idea of where you stand—and whether there are any areas for potential improvement.

If you’re working to improve your credit scores, you may consider getting pre-approved for a credit card that is tailored to those with fair credit and those looking to improve their credit.