How to read your credit card statement

Your credit card statement arrives each month, offering a detailed look at what’s going on with your credit card account. That makes your credit card statement a helpful tool to track spending, confirm payment details and identify unauthorized charges. In just a few pages, you might find topics from payments to rewards.

Learn more about how to read your credit card statement by seeing examples of what different sections of your statement might look like.

What you’ll learn:

-

If you have a credit card, the law requires your issuer to provide a monthly statement when there’s account activity.

-

Credit card statements might be mailed or provided digitally.

-

Statements are generally divided into different sections to provide information about payments, balances, transactions, interest and more.

-

Statements might also include account notifications, important information, terms and conditions.

What is a credit card statement?

Your credit card statement is a monthly record of your credit card activity. It gives you details on balances, account activity, interest, fees, rewards (if they’re offered) and more. It might also have notifications and updates about your account status.

How long is a credit card statement period?

A credit card statement typically covers a single billing cycle, which can last about 28 to 31 days. At the end of a billing cycle, your transactions and previous balances are added together to determine your statement balance.

The bill for your statement is usually due around three weeks later, although it depends on the credit card issuer. Then the next billing cycle begins right away.

Credit card statement example

A credit card statement can hold a lot of information. To make it easier to understand, it’s helpful to break it down into sections. While the following sections are fairly typical, they may not represent all statements.

Here’s a look at what you might find in your credit card statement:

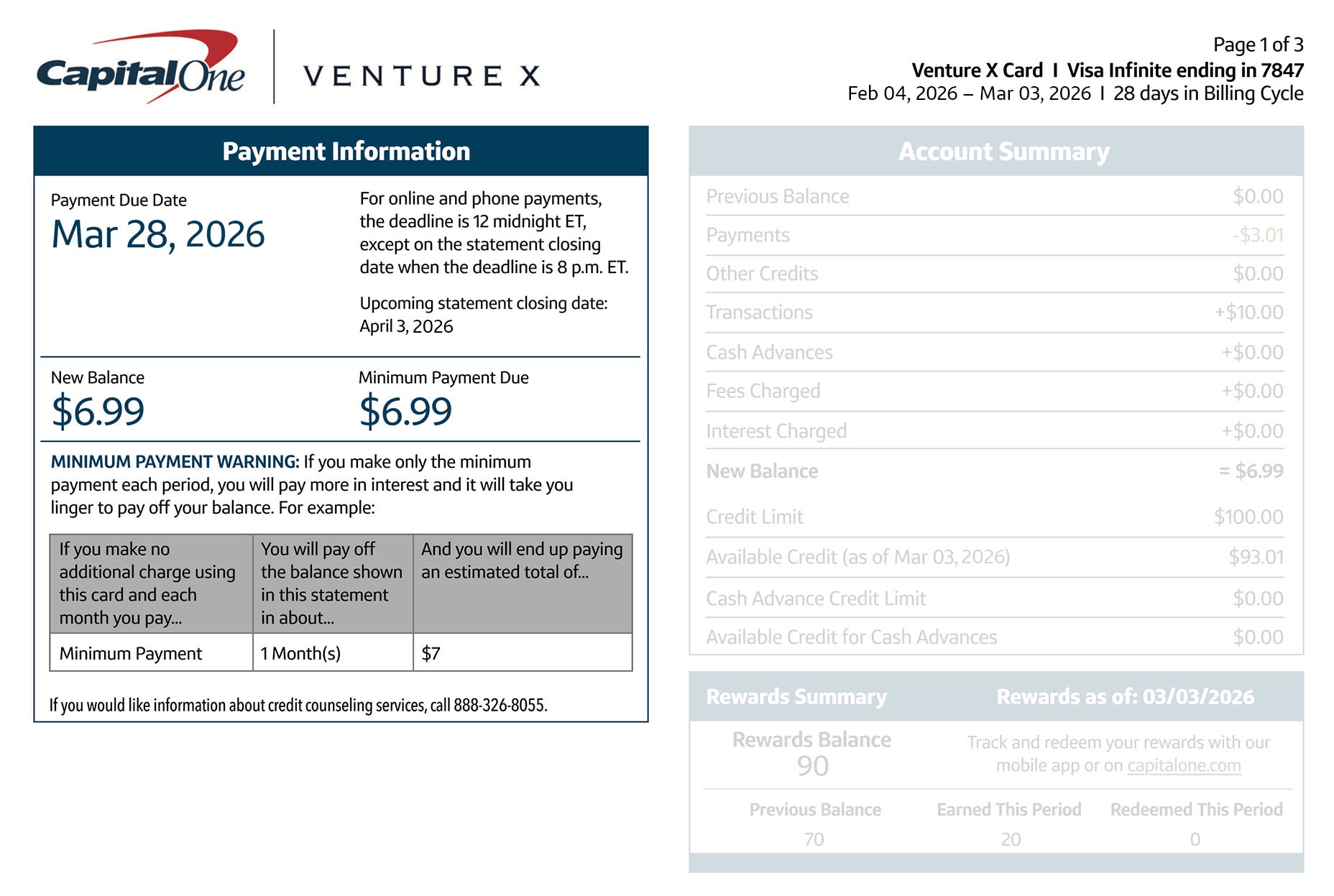

Payment information

A payment information box appears near the top of your credit card statement. Here, you’ll likely find:

-

Payment due date: A payment toward your balance must be made on or before this date.

-

New balance: Sometimes also called a statement balance, this is the total of the payments, credits, fees, interest and unpaid balances on your card since your last billing cycle.

-

Minimum payment due: If you’re unable to pay the full balance, you can pay at least this amount to avoid a late fee and keep your account in good standing. Just remember, by paying only the minimum payment, you could incur interest charges and increase the time it takes to pay off your balance.

-

Late payment warning: Depending on your issuer, you may be charged a fee for late payments. The late payment warning informs you of what that fee could be. Some issuers may also charge increased interest, which is sometimes called a penalty rate. If so, you may see that rate listed here as well.

- Minimum payment warning: The amount you pay each month can impact how long it takes you to pay off your balance in full. The minimum payment warning shows how long it would take to pay your balance using the minimum payment if you don’t continue to make transactions on your account. It also shows how much you could wind up paying in interest.

Account summary

The account summary provides a snapshot of your account activity during the latest billing period. Most summaries begin with your balance at the end of the last billing cycle. You may also see a reminder about your credit limit and how much credit you still have available. Other line items could include:

- Payments

- Credits

- Transactions

- Fees

- Interest charges

- Credit available for cash advances

Further down your statement, you might find more details about each of these in the Transactions section.

Rewards summary

If you have a rewards credit card, your statement might summarize your rewards. It might include:

-

Your current and previous rewards balance

-

Rewards earned during the current billing period

-

Rewards redeemed during the current billing period

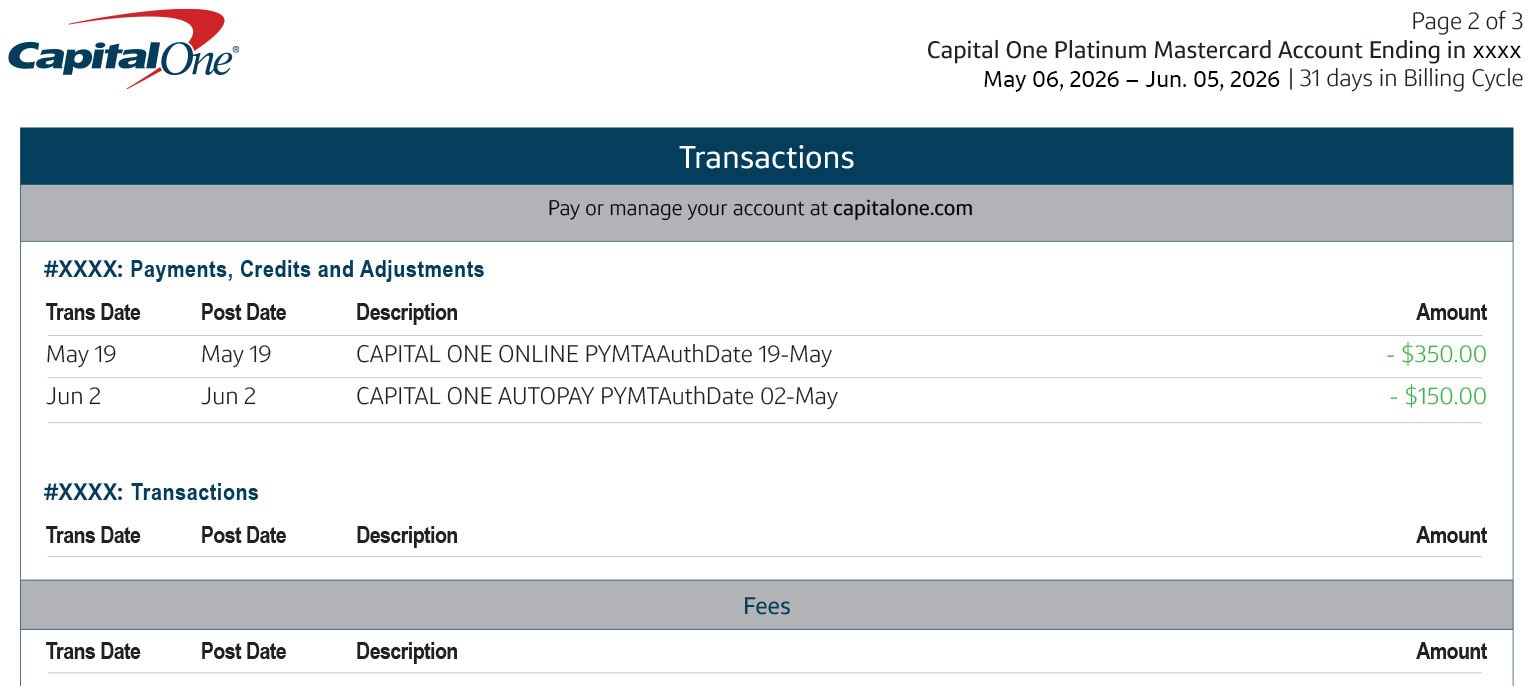

Transactions

The Transactions section is where a credit card issuer lists all the details of your account summary.

Depending on the issuer, you may see transactions grouped by date or type. Either way, this section will likely include:

-

Payments: This category includes any payments you made on your account during the last billing cycle.

-

Account credits: This can include refunds, earned rewards or mistakes that have been credited back to you.

-

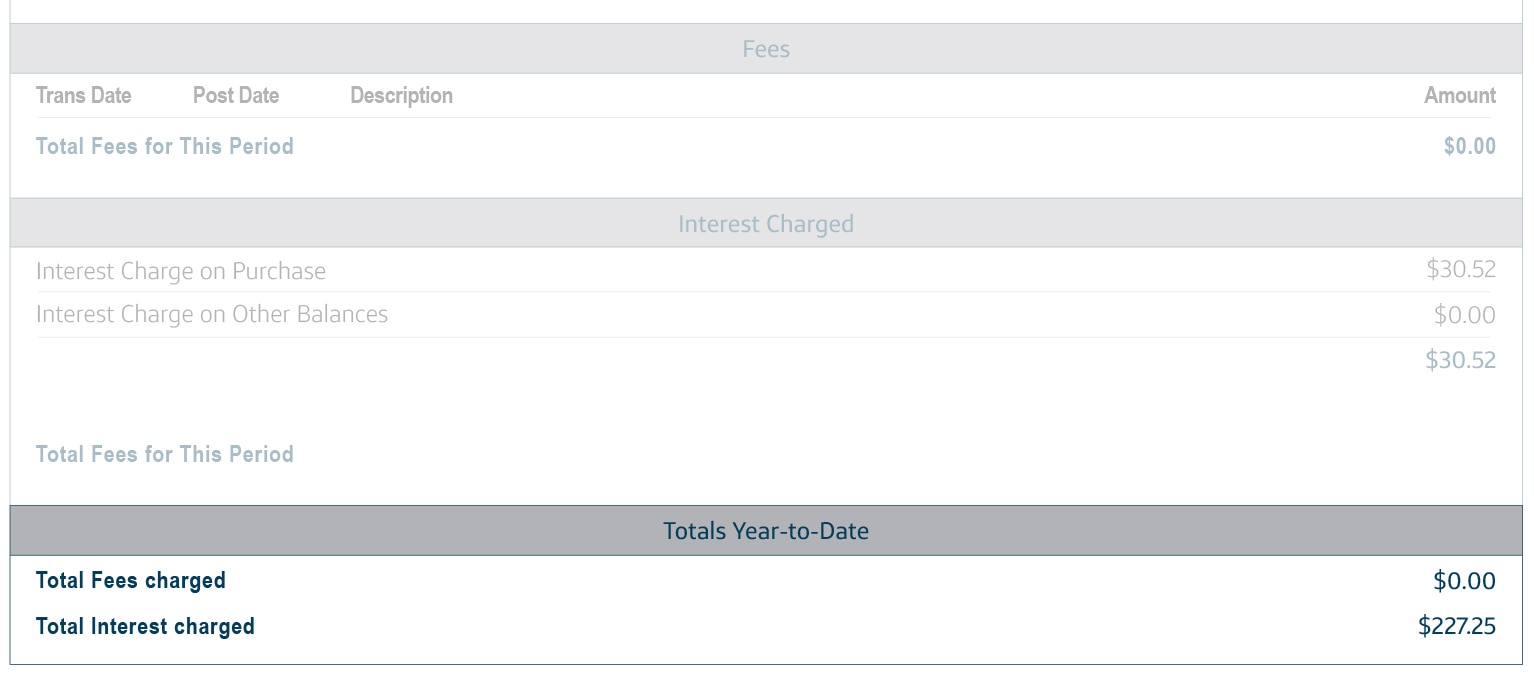

Fees: Issuers are required to provide details about any fees you owe. These could include things like late payment fees or your card’s annual fee. You may also see balance transfer or cash advance fees.

-

Interest charges: This category shows your total interest charges. This total could include interest charged if you carry a balance from a previous statement. It could also include interest that’s typically charged on transactions like cash advances and balance transfers, starting from the date of the transaction. Paying your balance in full every billing cycle can help you pay less in interest than you would if you carried over your balance from month to month.

-

Balance transfers: If you transferred a balance from another account to your credit card, that amount will be shown here.

- Cash advances: This details any cash you withdrew from your account via a cash advance.

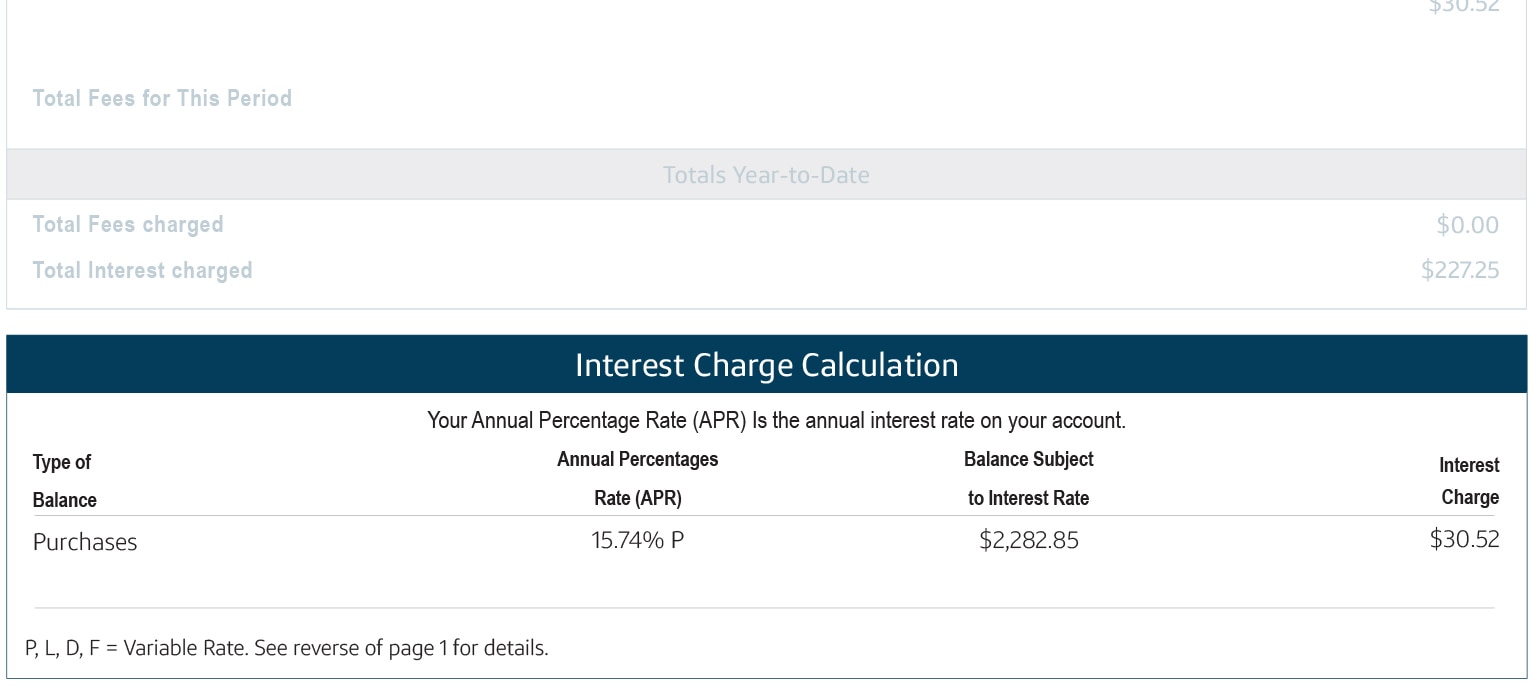

Year-end summary

This section shows how much you’ve been charged in fees and interest for the current year to date. This can be helpful to review as you’re budgeting for the year. It could also help if you’re looking for a snapshot of how much you’ve paid in addition to your balance. And remember, paying your full balance each month could help you pay less in interest and fees.

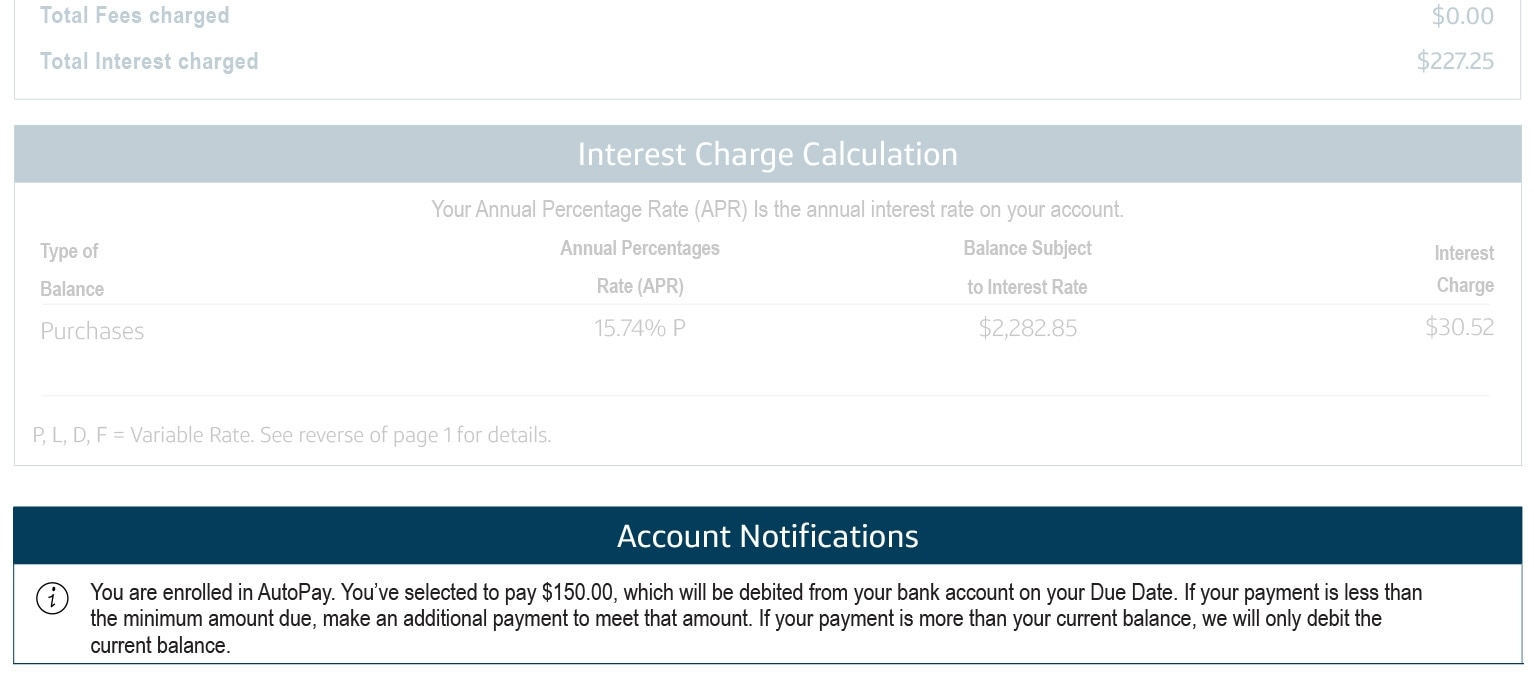

Interest charge calculation

This section is typically found near the end of your statement. It details your card’s interest rate, the balance on your account that is subject to that interest rate and the amount of interest charged.

Account notifications

The notifications section of your statement provides updates that may affect your account. If you’re a Capital One cardholder, you might see explanations of fees, interest charges or your AutoPay selections.

You might also see more general information. This could include how to contact customer service or use digital tools to find out about recent updates.

How can I access my credit card account statement?

Your credit card issuer should send you a monthly statement that aligns with your current billing cycle. Capital One customers can access their statements through the Capital One Mobile app or by signing in to their online account.

If you have a Capital One account, you can switch to paperless statements with just a few taps.

Where can I find my credit card statement balance?

You can typically find your balance in the account summary or payment information section of your statement. The summary section shows the charges and credits since your previous balance or the balance at the end of the last billing period. The payment information section shows the new balance, the minimum payment due and the payment due date.

How can I dispute billing errors?

If you spot an error on your credit card statement, the Fair Credit Billing Act says consumers typically have to report billing errors to their credit card issuer within 60 days of getting their statement. But sometimes it can be quicker to contact the merchant about the dispute first.

The Federal Trade Commission offers a sample dispute letter that consumers can use to notify the card issuer in writing.

How long do I keep credit card statements?

Based on how soon billing errors have to be reported, 60 days might be a good starting point to keep your statements. If you manage your account online, you may not need to keep any paper statements anywhere near that long. You can check with your issuer to learn more about how long it retains statements.

Key takeaways: Reading your credit card statement

Reading your credit card statement can help you stay on top of your spending and changes to your account.

If you’re interested, you could also compare Capital One credit cards, including their rewards, annual fees and more, and see if you’re pre-approved with no impact to your credit scores.