FICO® score vs. credit score: What’s the difference?

FICO scores are a type of credit score from credit-scoring company FICO.

Learn more about credit scores and FICO scores, including why they’re important, how they’re calculated and where you can find yours.

What you’ll learn:

-

Credit scores are used in lending decisions and are based on the information in credit reports.

-

A FICO score is one type of credit score calculated by the Fair Isaac Corporation (FICO).

-

FICO has multiple credit-scoring models that are used to calculate credit scores, including a variety of industry-specific models for mortgage lending, auto loans and more.

- FICO scores generally range from 300 to 850.

Is FICO score the same as credit score?

People typically have more than one credit score, because there are multiple credit-scoring companies. FICO is one example. And credit-scoring companies even have different credit-scoring models that are used to calculate different credit scores. FICO Score 8, which you’ll read about below, is an example of a credit score.

What is a credit score?

A credit score is a three-digit number that’s based on a borrower’s credit history and activity. Scores are based on the information in credit reports and are used to help determine a potential borrower’s creditworthiness. Lenders, credit card issuers and others use credit scores to judge loan and credit applications.

Scores can also affect the interest rates and credit limits cardholders are offered. And they can play a role in rental applications, insurance premiums and more.

How are credit scores calculated?

According to the Consumer Financial Protection Bureau, there are several factors that scoring models usually take into account when calculating credit scores, including:

-

Current unpaid debt

-

The number of loans a borrower has

-

The different types of loans a borrower has, which is known as credit mix

-

How long someone has had credit accounts

-

The amount of available credit someone is using, also known as credit utilization

-

Any recent applications for a new credit

-

Whether a borrower has had a bankruptcy, a foreclosure or a debt sent to collections—and how long ago it was

But remember that different companies have different scoring models. And some companies may have multiple versions of scoring models, which is why a person might have several different credit scores.

Different scoring models may consider certain aspects of your credit history or give more weight to certain factors. But regardless of the scoring model, the higher the score, the better.

What is a FICO score?

A FICO score is a credit score from the credit-scoring company of the same name. Shortened from Fair Isaac Corporation, FICO is one of two credit-scoring companies whose scores are most commonly used by lenders. The other is VantageScore®.

FICO is credited with creating the first standardized scoring model in 1989. Today, FICO offers a number of different scoring models to lenders, including FICO Score 8 and industry-specific scoring models, such as FICO Auto Scores and FICO Bankcard Scores.

How is a FICO score calculated?

Like other scoring models, FICO’s scores take a number of factors into account. They primarily consider your payment history, credit utilization, age and mix of accounts, and inquiries for new credit applications. And FICO is clear about how they weigh those factors when determining scores:

-

35% comes from payment history

-

30% is from credit utilization

-

15% comes from length of credit history

-

10% is from types of accounts, known as credit mix

- 10% is based on new hard credit inquiries

FICO score ranges

Like all credit-scoring models and companies, there are ranges to FICO scores. Typically, the range is 300 to 850. But specialty scores for banking and auto lending range from 250 to 900.

It’s important to remember that lenders ultimately decide what’s good when judging loan applications. Here’s a more detailed look at what FICO says about scoring ranges:

-

Exceptional: 800+

-

Very good: 740-799

-

Good: 670-739

-

Fair: 580-669

- Poor: less than 580

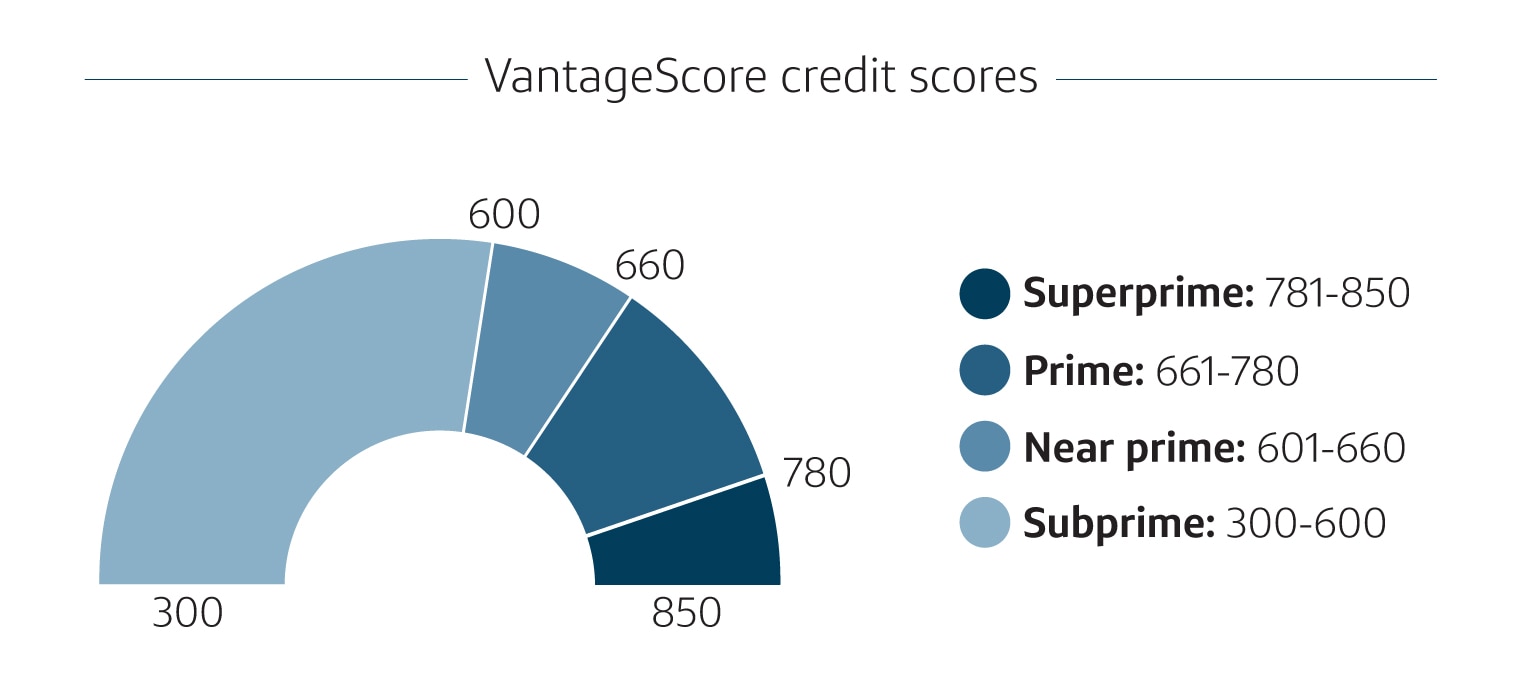

For comparison’s sake, VantageScore ranges generally look like this:

-

Superprime: 781-850

-

Prime: 661-780

-

Near prime: 601-660

-

Subprime: 300-600

You may notice that VantageScore uses different terminology to refer to their scoring ranges. Superprime represents the best scores you can have with VantageScore, but prime scores may still be considered good.

FICO vs. credit score FAQ

If you’re still learning about the differences between FICO scores and other credit scores, the answers to these frequently asked questions might help.

Is a FICO score accurate?

Credit scores are based on information from credit reports. So as long as the information in your credit reports is accurate, then your scores should reflect that.

If you’re not sure what’s in your credit reports, checking them regularly can be a good way to make sure the information is correct.

Are FICO scores or other credit scores more accurate?

No credit score is necessarily more accurate than another. That’s because your credit scores depend on the information in your credit reports, which gets reported to the credit bureaus by lenders and creditors.

But different credit-scoring companies and models may take different factors into account or weigh certain factors more heavily than others. And reports from different credit bureaus may not contain the exact same information. Those are a few reasons why you have different scores.

Why is my FICO score higher than my other credit scores?

Every credit-scoring model is different. And credit scores can change based on what credit report is used to inform the model. Those differences can make some scores higher or lower than others.

Even when a score is calculated can make a difference. For example, your credit scores might be higher after you pay your monthly credit card statement. One reason? Credit utilization, an important factor in scoring, might be lower at that time.

Why is my FICO score different on different sites?

The reason for the differences in scores comes down to the differences in credit reports from each of the major credit bureaus.

For example, lenders might not report credit activity to all three bureaus. So if a FICO score is calculated using a TransUnion® credit report on one site and an Experian® report on another, the resulting scores might vary.

Key takeaways: FICO scores vs. credit scores

Credit scores are three-digit numbers that are used in lending decisions. Scores are based on what’s found in credit reports, and they’re calculated by different credit-scoring companies using scoring models.

A FICO score is a credit score from FICO. And while the credit-scoring company has multiple scoring models of its own, FICO scores generally range from 300 to 850—with higher scores being better than lower ones.

If you want to check or track your credit, you can access free credit reports at AnnualCreditReport.com. Or you can consider CreditWise from Capital One. With CreditWise, you can access your credit report and credit score for free—without negatively impacting your scores. You can even see the potential impacts of financial decisions on your credit score before you make them by using the CreditWise Simulator. And CreditWise is available to everyone—even if you don’t have a Capital One credit card.