How to calculate your mortgage payment

Buying a home is a major financial decision. And when you’re looking at a home’s purchase price, it can be hard to figure out how much house you can afford. But if you’re using a mortgage, calculating your monthly mortgage payment may help you get your head around what you can realistically afford.

Find out how to calculate monthly mortgage payments, what costs are included and some potential ways to lower your monthly mortgage payment.

Key takeaways

- Monthly mortgage payments are made up of principal, interest and other costs, which might include homeowners insurance, private mortgage insurance (PMI) and property taxes.

- Calculating your monthly mortgage payment may help you set a budget and narrow your search.

- You can use online mortgage payment calculators or a mathematical formula to calculate monthly principal and interest costs.

- If you’re looking for ways to lower monthly mortgage payments, you can explore options like refinancing or recasting, extending the loan term, getting rid of PMI, or finding lower-cost insurance.

What costs are included in a mortgage payment?

Principal and interest are two major parts of a monthly mortgage payment. The principal goes toward paying back the money you borrowed. The interest is the price you pay for borrowing that money.

But you can’t always get a complete picture of what you’ll owe each month by only looking at those two costs. You also have to consider any other costs that may be rolled into your monthly mortgage payment, including:

- Homeowners insurance premiums

- PMI premiums

- Property taxes

Your lender will generally keep these parts of your monthly payment in an escrow account and then pay the bills on your behalf. If your home comes with HOA fees, remember to include those in your monthly payment calculation too, though you may have to pay them separately.

Down payments

The size of your down payment also affects your monthly mortgage payment. A larger down payment means a smaller starting loan balance. And that generally means you’ll have to pay less principal and interest over the course of the loan.

Down payment size can also affect whether you need PMI or not. For conventional mortgage loans, lenders typically require PMI when a borrower puts down less than 20% on a home. All FHA-backed loans require a different kind of mortgage insurance called a mortgage insurance premium.

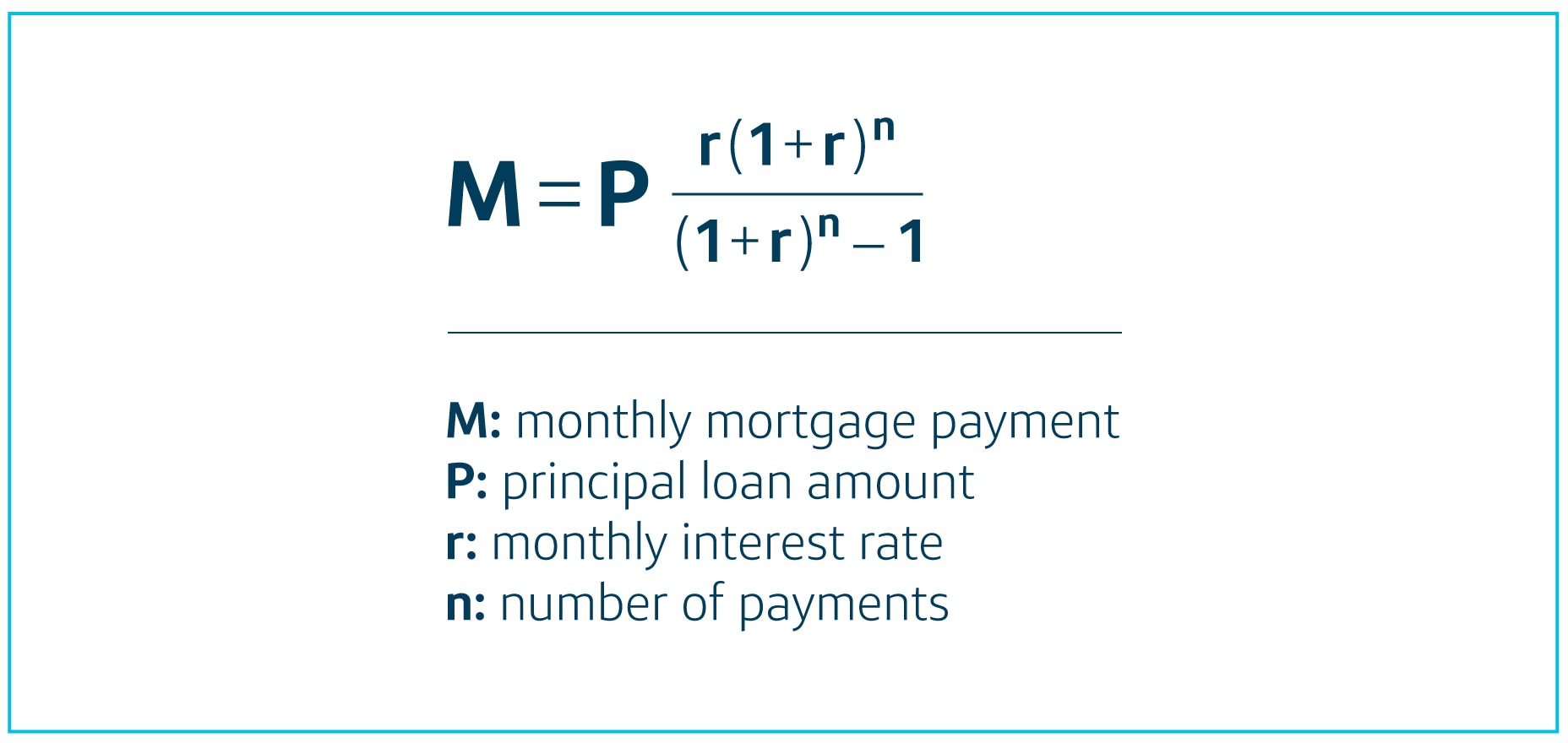

Mortgage payment formula: How to calculate your monthly cost

You can use the formula below to find out how much principal and interest you’ll need to pay each month. The formula is pretty complex. If math isn’t your thing, consider finding a mortgage payment calculator online to help you out.

Here’s how that formula breaks down:

- M = Monthly mortgage payment.

- P = Principal loan amount. This is the total amount you borrowed.

- r = Monthly interest rate. You can calculate this by dividing your annual interest rate by 12.

- n = Number of payments you’ll need to make over the life of the loan. You can find this by multiplying the number of years in your loan term by 12.

Remember that this formula only shows what your principal and interest costs will be. Don’t forget to add in any other costs that may be included in your monthly payment, like taxes, insurance and fees.

Your lender may also give you a loan amortization schedule that shows you how your monthly payments will be divided between interest and principal over the loan term. The Consumer Financial Protection Bureau also notes that if you receive any written loan estimates before you decide on a mortgage, they may include an estimate of your total monthly payment.

How to calculate mortgage interest

How much interest you’ll owe on your monthly mortgage payment can depend on whether you have a fixed-rate mortgage or an adjustable-rate mortgage. It may also depend on the type of loan and the loan term. For example, you’ll typically pay less interest on a loan with a shorter term. But the monthly payment may be higher.

You can use the mortgage payment formula or online calculators to help estimate your monthly interest charges.

Why is it important to calculate your mortgage payment?

Calculating your monthly mortgage payment can help you narrow down your search to homes you can afford.

Breaking things down month by month can also help with creating a monthly budget. This way, you’ll know how much of your monthly income will be going toward your mortgage payment. And then you can decide whether that will work with your lifestyle and financial goals.

Don’t forget to think through other costs of owning a home, like renovations, repairs, moving costs, utilities and closing costs, too.

Can you lower your monthly mortgage payment?

There are a few ways you may be able to lower your monthly mortgage payment. But whether these options are available to you depends on things like your lender, loan and specific circumstances. Here are a few possibilities to explore:

- Refinancing or recasting the mortgage

- Extending the loan term

- Getting rid of PMI

- Finding a lower-cost homeowners insurance policy

Make sure you fully understand the ramifications of these options before making any decisions. It may also be helpful to talk to your lender or a qualified financial professional to help you determine what’s right for you.

Calculating mortgage payments in a nutshell

Figuring out how much you may owe on a mortgage each month can help you set a budget and narrow down your search to homes you can realistically afford.

If you want to find out where your credit score stands before applying for a mortgage, check out CreditWise from CapitalOne. With CreditWise, you can access your credit report and credit score anytime without hurting your credit scores.

You can even explore the potential impact of financial decisions, like getting a mortgage, before you make them with the CreditWise Simulator. CreditWise is free for everyone, whether you’re a Capital One customer or not.