The advantages of the classic savings account

Why this tried-and-true method for saving still works

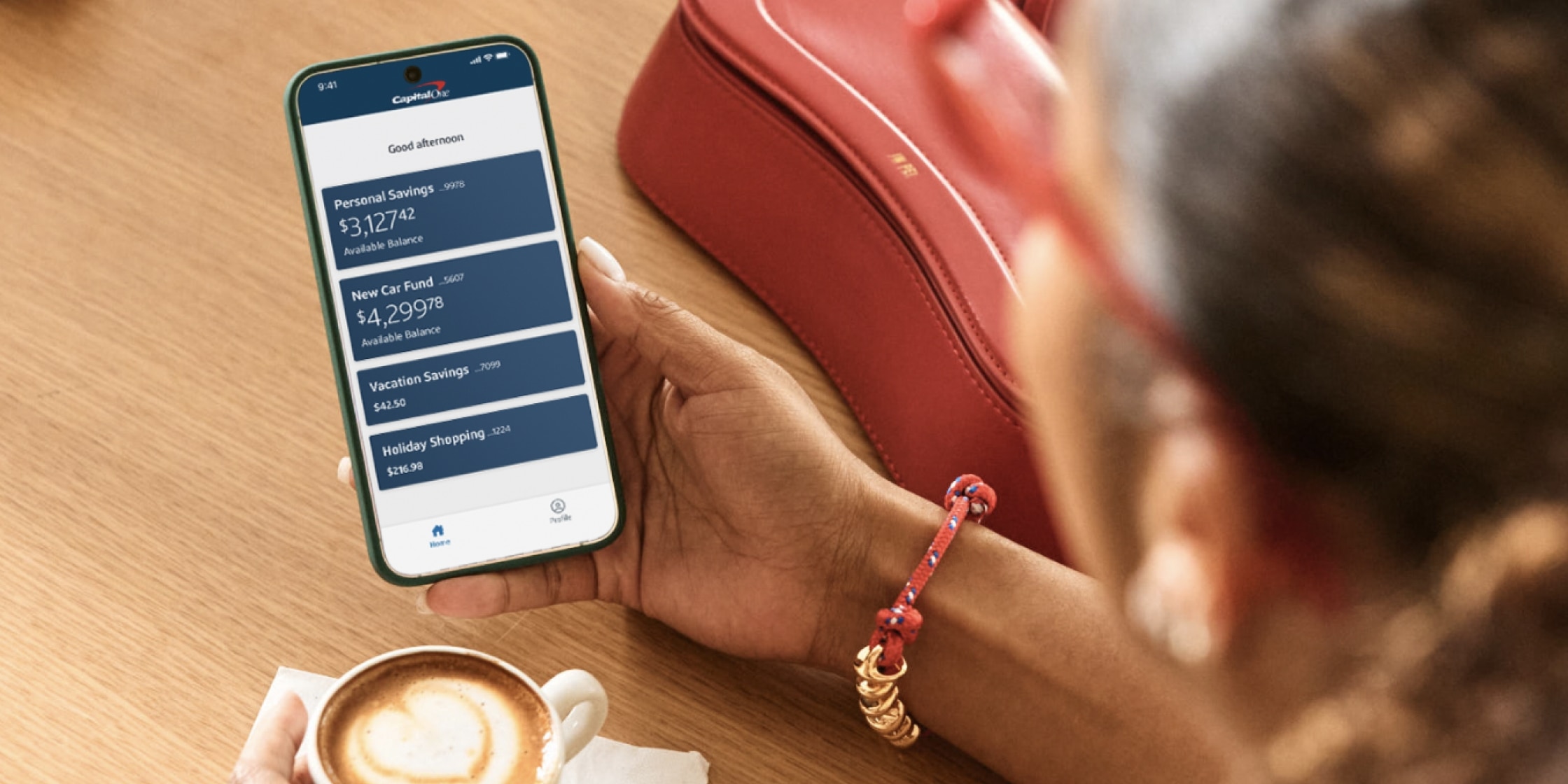

Your paycheck is deposited directly into your bank. You pay for your coffee with your smartphone and thumbprint. Dinner? You order delivery from your favorite restaurant with a few taps of a finger.

If you’re tech-savvy when it comes to handling your money, you may wonder whether or not a more traditional option like a savings account could benefit you.

People have been using savings accounts since long before ATMs and online banking existed, but there are still advantages to saving money the “classic” way. Even in a modern world with so much financial technology (often called “fintech”), the benefits of a savings account are clear: Your money is safe, secure and growing.

If you’re interested in saving for your future, you’re already on the right track. Understanding the advantages of a savings account and how it can help you meet your money goals is the next step.

Checking accounts vs. savings accounts

If you’ve already got a checking account, opening a savings account might sound redundant. But once you understand the differences between a checking and savings account, you’ll see how these 2 types of accounts can help you reach your money goals in different ways.

One of the main differences between checking and savings accounts is accessibility.1 A checking account is designed to keep your money handy for withdrawal or for everyday purchases using a debit card. This can be a good place to store your spending money and the cash you need on hand for bills, rent or mortgage payments.

A savings account, on the other hand, is designed for saving instead of spending. It keeps your money a little less accessible so you’ll be motivated to save while keeping it in reach if you need it. While some savings accounts can be attached to debit cards or checks, they’re not typically used for everyday purchases like groceries and car washes. When your money is in a savings account, you can’t easily spend it on everyday purchases just by swiping a card, which can help you save.

Homeowner’s or renter’s insurance can give you the peace of mind of knowing you’ll be covered should something happen to your home. Putting money in a checking account or savings account works in a similar way. In a bank, your money is safe because it’s insured by the Federal Deposit Insurance Corporation (FDIC).2

The benefits of a savings account

Keeping your money safe and secure is just one of the benefits of a savings account. Another bonus is that the cash you put into a savings account earns interest. Interest is money paid to you by the bank at a specific rate. Money in a savings account typically earns more interest than it would in a checking account.3

You could also benefit from compound interest. Here’s how that works: When your bank pays you interest, the money they give you increases your balance. The next time they pay you interest, it’ll be based on that new, larger balance. This means the bank is actually giving you a percentage of the money they’ve already paid you. It’s a great way to grow your savings without even making a deposit.

When shopping for interest rates on savings accounts, look for a competitive rate that will help you get the most out of your hard-earned money. Remember, even 1% of $5,000 is $50. That’s an extra $50 the bank gives you just for saving your own cash. Think of it as a night out at the movies, an extra tank of gas or a holiday gift for a loved one courtesy of your bank.

When considering the pros and cons of savings accounts, another thing to factor in is fees. Some banks may charge fees to open an account or monthly maintenance fees. There may also be minimums to open an account.4

Making the most of your savings account

Once you open a savings account, you can start to take advantage of its features to further your savings goals.

One option is to set up automatic savings transfers. When you do that, a set amount of money of your choice will be withdrawn from your checking account or paycheck and transferred to your savings every month just like other auto-pay bills. Automatic transfers are an easy way to keep you on track. After you set it up, the bank handles the rest for you, so you can stick to your savings goals easily.

Like a black dress or a great pair of jeans, you can’t go wrong with a classic. Even in today’s fast-paced “fintech” world, the savings account is still a reliable way to protect your money, earn a little interest and save for your future.