What credit score do you start with?

When you check your credit scores for the first time, you might be surprised to find a three-digit number, even if you’re new to credit. That’s because your credit score doesn’t start at zero.

Read on to learn more about where your score starts and why using credit responsibly is important from day one.

What you’ll learn:

-

There isn’t a set credit score that each person starts with. Instead, if you don’t have any credit history, you likely don’t have a score at all.

-

Credit scores are calculated based on factors such as payment history, current debt, credit utilization, credit mix, credit age and new credit applications.

-

Once credit is established, credit scores typically range from 300 to 850.

What is your starting credit score?

There’s no specific credit score everyone starts with. And you can have different credit scores depending on the credit-scoring model from credit-scoring companies, such as FICO or VantageScore.

But you won’t start with a score of zero. You simply won’t have a score at all. That’s because your credit scores aren’t calculated until a lender or another entity requests them to determine your creditworthiness.

When does your credit score start?

Taking out your first credit card or other line of credit often marks the start of a person’s credit history. It typically takes some time—about six months—for credit bureaus to gather enough information for credit reporting companies to determine your starting credit score.

The key is learning how to use credit responsibly to help build the best score possible.

How is your starting credit score calculated?

According to the Consumer Financial Protection Bureau (CFPB), here are some factors that have a direct impact on your credit scores:

-

Payment history: Your payment history indicates how well you’ve made payments on time.

-

Debt: This refers to how much current unpaid debt you have across all your accounts.

-

Credit utilization: This is the ratio that reflects how much of your available credit you’re using compared with how much you have available. Credit utilization is usually expressed as a percentage.

-

Credit mix: Your credit mix refers to how many and what kinds of loans you have, such as revolving credit accounts and installment loans.

-

Credit age: It represents how long your accounts have been open.

-

New credit applications: This reflects how many times you’ve recently applied for new credit. The effect of a single application might be minor. But a lot of new applications, each of which triggers a hard credit inquiry, could give a negative impression to lenders.

How exactly these factors affect your scores depends on the credit-scoring model, a mathematical formula used by the company calculating your score. A model might use information from a combination of different credit reports or from just one report. Then, each credit-scoring model might assign different levels of importance to that information.

Credit score ranges

FICO and VantageScore are the two credit-scoring companies that provide some of the most commonly used credit scores. Scores from both companies range from 300 to 850.

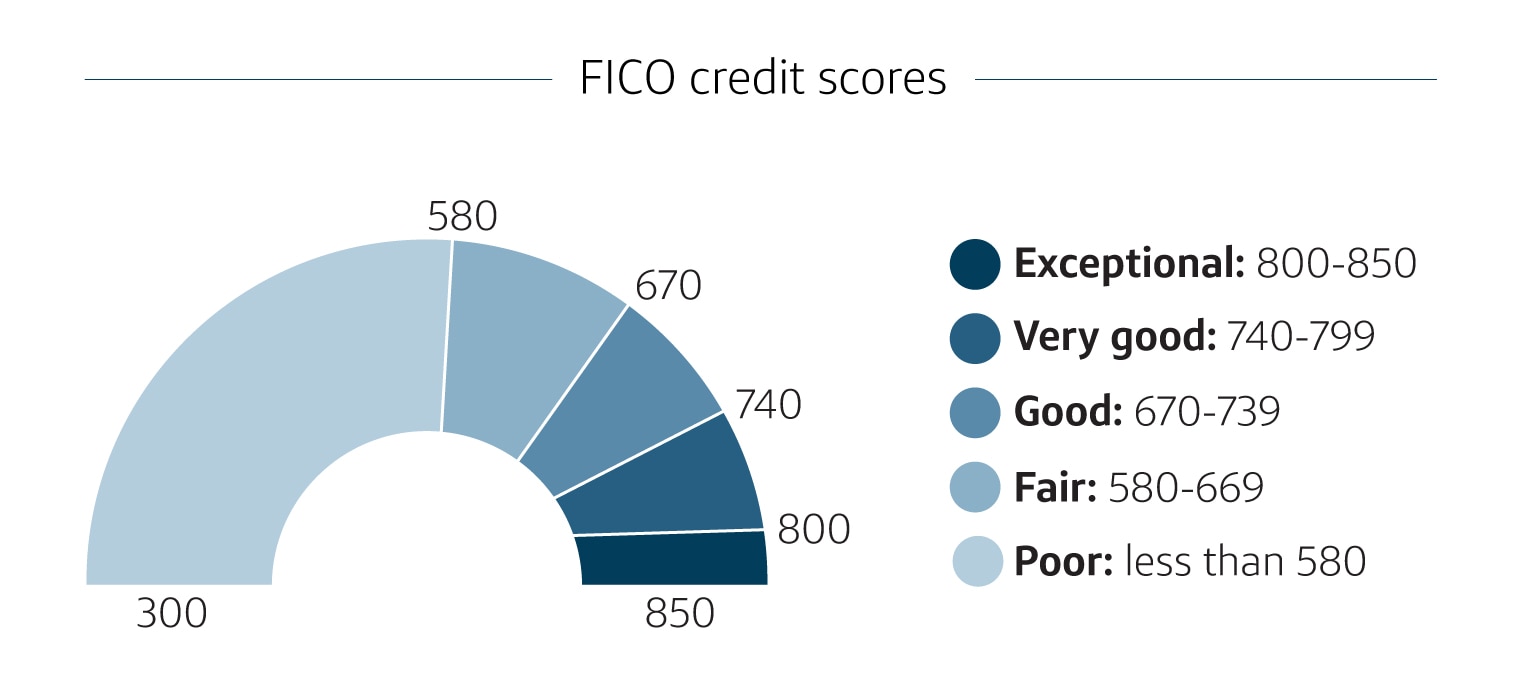

FICO credit score ranges

Here’s how FICO categorizes its scores:

-

Exceptional: 800+

-

Very good: 740-799

-

Good: 670-739

-

Fair: 580-669

- Poor: Less than 580

Source: MyFICO.com.

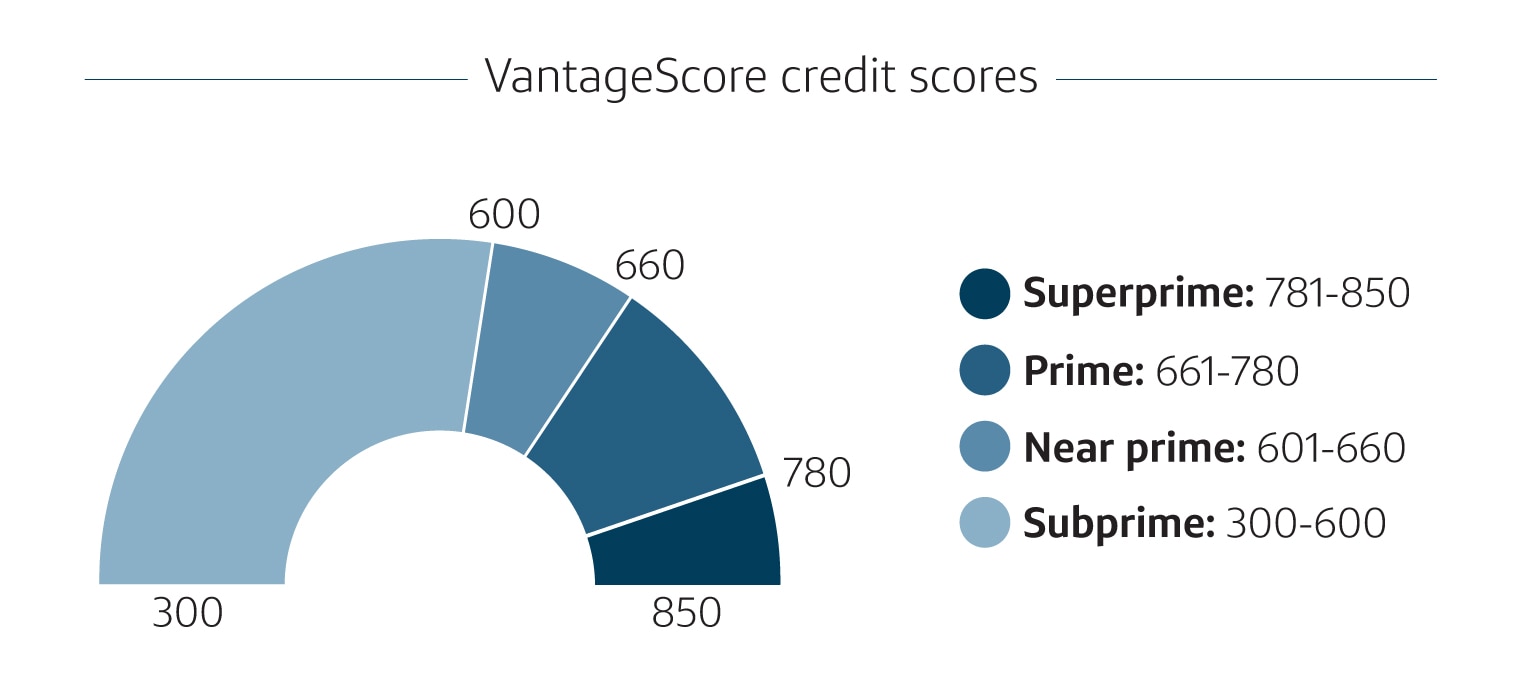

VantageScore ranges

Here’s how VantageScore categorizes its scores:

-

Superprime: 781-850

-

Prime: 661-780

-

Near prime: 601-660

- Subprime: 300-600

Source: VantageScore.com.

At what age does your credit score start?

Most people likely won’t have credit reports or scores before turning 18—or even 21. That’s because of laws that determine when a person can get loans or credit cards of their own.

But if a trusted family member or friend adds you as an authorized user, it could help you establish credit earlier if the account is used responsibly.

How to establish and maintain good credit

Building credit is a process. But there are certain things you can do to build credit for the first time.

-

Apply for a credit card and use it responsibly: If you don’t have a credit history, you might want to consider applying for a secured credit card, which involves giving a refundable deposit to the credit card issuer. You might even be eligible for a traditional card. See if you’re pre-approved with no impact to your credit scores.

-

Become an authorized user: If a trusted family member or friend has good credit, you could ask them to add you to their account as an authorized user. Becoming an authorized user allows you to make purchases, but the primary cardholder is ultimately responsible for all the charges made on the account. Keep in mind that things like late payments can hurt both users’ credit scores.

- Take out a credit-builder loan: Credit-builder loans allow you to build your credit history. The lender deposits the loan amount in a locked savings account, and you make set payments over a fixed amount of time to pay it back. Payments are reported to credit bureaus to help you establish credit. And once the loan is paid off, you get the money back.

Is it possible to have a credit score without a credit card?

To establish a credit score, you’ll still need to have a line of credit or loan associated with your name. There are different types of credit, including revolving credit and installment loans.

A credit card is an example of a revolving credit account. So are home equity lines of credit and personal lines of credit. Mortgages, car loans, personal loans and student loans are examples of installment credit.

How to monitor your credit score

You can get free copies of your credit reports from all three major credit bureaus—Equifax®, Experian® and TransUnion®—by visiting AnnualCreditReport.com.

CreditWise from Capital One

CreditWise is a free tool that lets you monitor your credit report and credit score. Using CreditWise won’t hurt your credit scores. And it’s free for everyone—not just Capital One cardholders.

Starting credit score FAQ

Here are some frequently asked questions about starting credit scores.

Will my credit score start at the lowest possible score?

While the lowest score possible from FICO or VantageScore is 300, your score won’t automatically start there.

How long does it take to go from your beginning credit score to good credit?

It can take about three to six months to get your first credit score after you’ve opened at least one credit account. But it takes time and responsible use to build your credit scores.

How do you know your credit score is accurate?

You can ensure your credit score is accurate over time by regularly monitoring your credit reports. If you find any inaccurate information, contact the credit bureau where it was listed to take steps to have that information corrected or removed.

Key takeaways: Starting credit scores

Even if you haven’t had any type of credit before, your scores don’t start at zero.

As you begin your credit journey, remember there are ways to start positive financial habits right away to help you continue building better scores. And if you’re considering applying for a credit card, compare Capital One credit cards or see if you’re pre-approved today.