What is a fair credit score?

Most credit scores fall between 300 and 850. Depending on where yours fall within that range, your credit might be considered excellent, good, fair or poor. As far as what’s considered a fair credit score, that range is typically between 580 and 669 depending on the scoring model used.

Keep reading to learn how to tell whether you have a fair credit score, why credit scores are important and what you can do to help improve yours.

What you’ll learn:

-

A fair credit score typically falls somewhere between 580 and 669, depending on the scoring model.

-

Improving your credit scores can help you become eligible for credit cards with better rewards programs and better loan terms.

-

Responsibly using a secured credit card is one way to help build credit.

-

If your credit is considered fair, paying bills on time every month and managing your credit responsibly can help improve your scores.

What is fair credit?

What’s considered fair credit may differ slightly based on what credit-scoring company the scores came from. You can see the differences in models from two commonly used companies:

-

FICO® says a fair credit score is between 580 and 669.

-

VantageScore® says near prime or fair scores fall between 601 and 660.

Ultimately, it’s up to lenders to decide for themselves whom to extend credit to and on what terms. But if you’re interested in how scores are classified by the two major credit-scoring companies, FICO and VantageScore, take a closer look below.

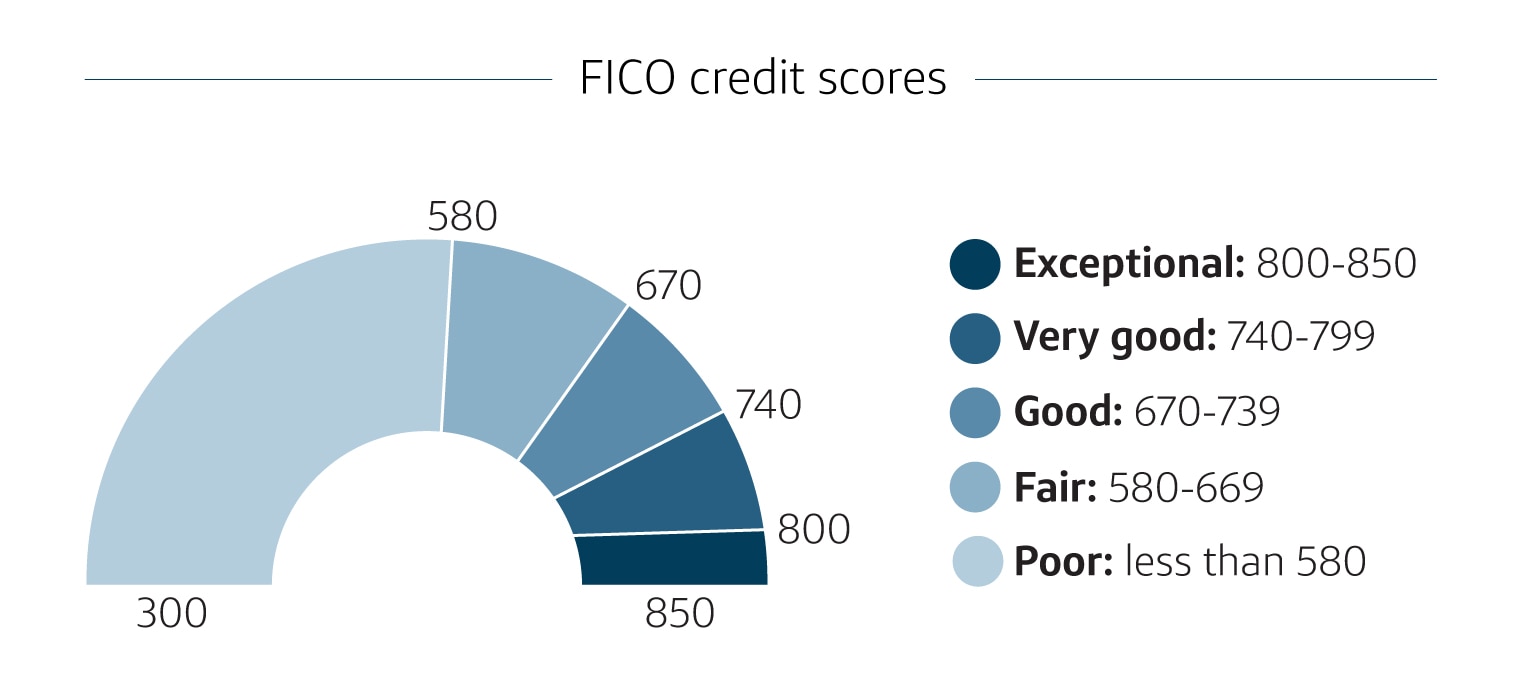

Fair FICO credit scores

Here’s how FICO categorizes its scores:

-

Exceptional (800-850): Borrowers in the exceptional credit score range are the most likely to qualify for credit and get good interest rates, according to Experian®, a major credit bureau.

-

Very good (740-799): FICO says borrowers in this category also tend to have higher-than-average credit scores. That makes it easier to qualify for favorable credit terms.

-

Good (670-739): Lenders are generally willing to extend credit to people with good credit scores because they’ve typically proven they will repay borrowed money.

-

Fair (580-669): While credit scores in the fair range are below average in the U.S., lenders may still approve borrowers for credit products. Options could be more limited, though.

- Poor (300-579): Applicants with credit scores in this range may be turned down for credit requests. Or the lender may approve the application but require a fee or deposit upfront.

Source: MyFICO.com

Keep in mind that scoring companies have different versions of scores. And that could result in slight differences in how scoring ranges are reported.

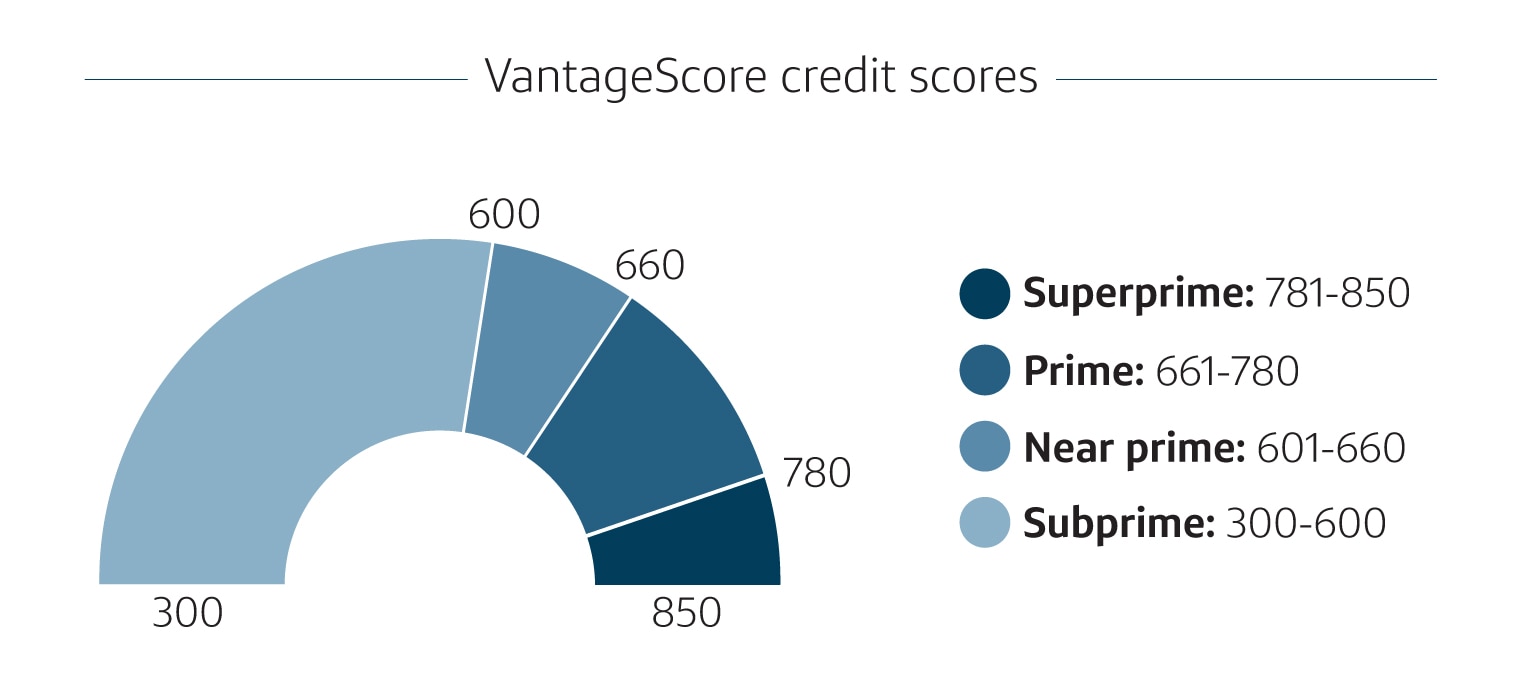

Fair VantageScore credit scores

VantageScore’s scale is slightly different from FICO’s. Here’s how VantageScore says its scores might be judged:

-

Superprime (781-850): This is the best category possible for VantageScore. Potential borrowers with excellent credit are usually trusted to repay what they borrow.

-

Prime (661-780): Prime credit is considered good credit. People with scores in this range are unlikely to have trouble getting approved for loans.

-

Near prime (601-660): It could be more difficult for people with near prime or fair credit scores to be approved for loans or credit cards. And loan approvals may come with higher interest rates.

- Subprime (300-600): Having a credit score in this range could mean higher interest rates if a loan is approved at all. But there are ways to improve your scores.

Not sure if you have a near prime credit score? You can check your score by using CreditWise from Capital One—even if you’re not a Capital One cardholder. Best of all, it’s free for everyone, and you can check as often as you like without hurting your credit scores.

Fair credit vs. good credit: What’s the difference?

Fair credit scores generally fall near the middle of credit score ranges. And good credit scores are a step above fair scores.

A good FICO score falls between 670 and 739, while VantageScore’s range for good or prime scores is from 661 to 780.

The better your credit is, the better a candidate you may be for things like credit cards and loans. But that’s just the start. Here are a few reasons why having strong credit is important:

-

Credit cards: A higher credit score may improve your chances of qualifying for a credit card that best fits your situation—whether you’re looking for a good rewards program or a low APR.

-

Mortgages and other loans: Strong credit can also help you qualify for mortgages, auto loans, personal loans and more.

-

Interest rates: If you qualify for a loan or credit card, the lender may also use your credit score when deciding your interest rate or credit limit. Generally, a higher credit score could help you get better terms.

-

Rental applications: Landlords may pull your credit report to help them decide whether you qualify for an apartment lease.

-

Employment applications: With your written permission, employers may pull your credit reports during a background check.

-

Insurance premiums: Depending on state laws, insurers may consider your credit history when determining premiums.

-

Deposits: Cellphone providers and utility companies may decide to waive security deposits for people with strong credit.

These are just a few of the reasons higher credit scores can be so valuable. If you’re not satisfied with your scores, there are things you can do to help improve them.

Which Capital One cards can you apply for with fair credit?

The better your credit, the more options you’ll likely have when applying for a credit card. But even if you have fair credit, you still have options.

Capital One has credit cards that are geared toward applicants with fair credit scores, including Platinum, QuicksilverOne and SavorOne.

Steps to help improve your fair credit score

While you may qualify for loans with fair credit, improving your scores could help you get more favorable terms. Here are a few steps you can take to help you work toward a better credit score:

-

Use credit responsibly. There are several ways to show lenders you’re a responsible borrower, like paying your bills on time every month. This shows lenders you’re following the terms of your agreement. Also, try to keep your credit utilization low. The Consumer Financial Protection Bureau (CFPB) recommends doing this by keeping your credit card balances at no more than 30% of your available credit card limits across all accounts.

-

Avoid payment mistakes. Payment history is a key credit-scoring factor. And late payments can lead to lower scores. Credit aside, you could end up being charged more in interest or fees too. Plus, paying only the minimum amount due or maxing out your credit limit can keep your credit utilization ratio high and bruise your credit.

-

Consider applications. Opening too many new credit accounts within a short period of time could hurt your scores because credit-scoring formulas take recent credit inquiries into account. It could also give lenders a negative impression of your personal finances.

-

Monitor your credit. Checking your credit reports regularly can help ensure that the information used to calculate your credit scores is accurate. You can take a look at your report anytime through CreditWise. And you can get free copies of your credit reports from each of the three major credit bureaus—TransUnion®, Equifax® and Experian®—at AnnualCreditReport.com.

-

Consider a secured credit card. A secured credit card can be a great tool for those with fair credit or low scores. Secured cards require a security deposit to open the account, which is why they’re typically easier to be approved for. But like a credit card, a secured credit card can help build credit if used responsibly.

- Beware of quick fixes. Remember that credit repair and credit building take time. There’s no such thing as a quick credit fix. But it’s never a bad time to start developing good habits to help improve your credit.

Fair credit scores FAQ

Here are the answers to a few frequently asked questions about fair credit scores:

Is a fair credit score okay?

Remember: The higher your credit scores, the better. Higher credit scores can make it easier to qualify for credit—and the better your terms are likely to be.

What can you do if your fair credit scores drop to poor?

If you see your scores drop from fair to poor, try to identify the reason for the drop. Are you making payments on time and in full? Are you carrying a balance or maxing your credit card out each month? Once you know the cause, you could start trying to improve your scores by paying down what you owe and using your credit card responsibly.

Is a 600 credit score considered fair?

A 600 credit score is considered fair by FICO or near prime by VantageScore.

Key takeaways: What is a fair credit score?

Fair credit scores typically fall between 580 and 669. And while you can qualify for credit with fair credit scores, higher scores typically mean more options and better terms.

Ready to kick-start your credit-building journey? Compare Capital One’s credit cards for fair credit and get pre-approved today to see which card may be the best fit for you. Getting pre-approved for a Capital One credit card only takes a few minutes—and it won’t impact your scores.