8 benefits of having a good credit score

Good credit. You may’ve heard the term more times than you can count. There’s a reason for that.

It’s because credit can touch many parts of your life. For example, it may impact where you live, how much money you can borrow and how certain employers may view your job application. Read on to take a closer look at the benefits of good credit and how you could work on improving your own.

What’s a good credit score?

A good credit range depends on where a score comes from and who’s judging it. And there are different scoring companies, so you can have more than one credit score. As the Consumer Financial Protection Bureau (CFPB) puts it, “Based on your credit reports, you will be given a credit score by the credit-reporting companies. You don’t just have one credit score—each company does their own.”

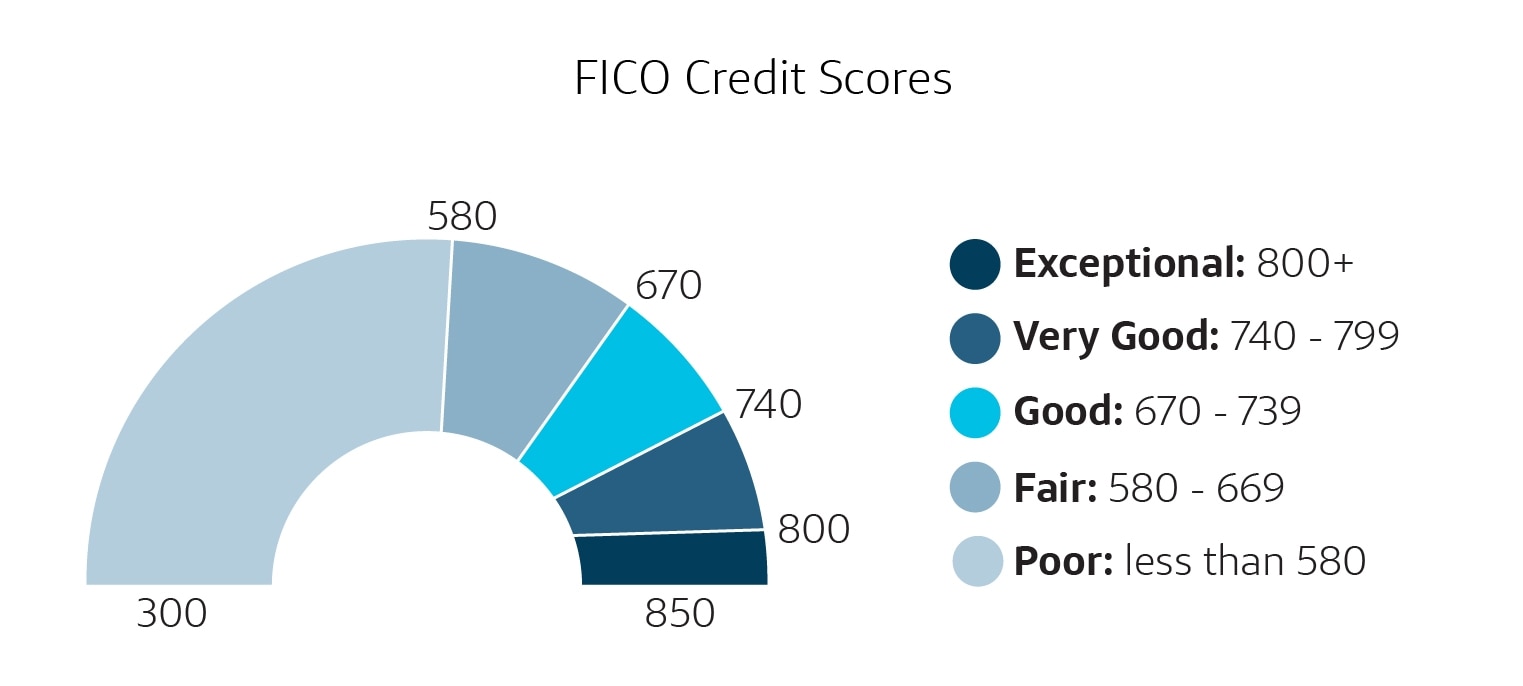

FICO®, which is one credit-scoring company, says scores between 670 and 739 qualify as good. For VantageScore®, another credit-scoring company, scores between 661 and 780 might be considered good. Scores can also be considered very good, excellent and exceptional.

It may also help to know that credit scores are based on information in your credit reports. Scores are calculated by credit-scoring companies, like FICO and VantageScore, using complex formulas called scoring models.

Here’s how FICO and VantageScore define credit score ranges:

Source: MyFICO.com

Source: VantageScore.com

What are the benefits of a good credit score?

The benefits of good credit can include everything from lower credit card interest rates to lower car insurance premiums.

Since credit scores are based on information in your credit reports, a higher score is a sign of healthy credit—and that can be the key to enjoying these eight benefits:

1. Get better rates on car insurance

First up: car insurance. Some insurance companies may use your credit scores to make all kinds of decisions when you apply for coverage.

According to the CFPB, insurance carriers can use your credit reports to help decide whether to approve your application and how much to charge you. Once you’re a customer, they may check your credit to help decide whether to raise your premiums or even deny you the chance to renew your policy.

2. Save on other types of insurance

Companies offering other kinds of insurance—home insurance, for example—may also look at your credit history.

That’s because insurance companies may want the same information that other lenders look for. That could include your history of on-time bill payments as well as how much debt you owe. What insurance companies learn about your credit may help them determine how much you’ll pay in premiums.

3. Qualify for lower credit card interest

When you apply for a credit card, the card issuer will likely check your credit. If you’re approved, a good credit score may make you eligible for things like a lower annual percentage rate (APR).

What exactly is an APR? The CFPB describes it as the price you pay for borrowing money: “For credit cards, the interest rates are typically stated as a yearly rate. This is called the annual percentage rate (APR).” The CFPB also says that good credit may be helpful when it comes to determining your APR since “credit card companies typically offer their best rates to customers who have the highest credit scores.”

Good credit may also play a role when you want to upgrade or apply for a new credit card—one with better benefits and rewards, for instance.

4. Get approved for higher credit limits

You’ve just learned about how good credit may help you qualify for lower interest on credit cards. It may also help you get a higher credit limit on credit cards.

Finally, good credit may also help you get bigger loans—from banks, for instance. Since a good credit score may signal to lenders that you’re a good credit risk, they may be willing to lend you more money.

5. Have more housing options

Where you live can have a big impact on your quality of life, right? Good credit can help in this instance too. That’s because landlords may check your credit history when you apply to rent an apartment.

Good credit may also help you get a mortgage for a house and a lower interest rate. The CFPB says, “The better your credit history, the more likely you are to receive a good interest rate on your mortgage loan.”

6. Get utility services more easily

Your credit may also be considered when you set up accounts for utilities like electricity or internet service. According to the Federal Trade Commission, “Getting utility services…has a lot to do with your credit history. The better your credit history, the easier it will be for you to get services.”

Also, good credit can mean that the utility company might not require a security deposit.

7. Get a cell phone without prepaying or making a security deposit

If you have poor credit, some cell phone companies may require a security deposit or ask you to prepay when opening your account. But good credit may help you avoid those up-front costs.

8. Look better to potential employers

When you apply for a job, some companies may look at your credit reports as part of a background check. While it’s possible to get a job with less-than-perfect credit, employers might see things like late payments and bankruptcies as possible red flags.

That’s why the CFPB recommends checking your credit reports before you start looking for a job. Checking your reports may help you spot mistakes and missing information. You can get free credit reports from each of the three major credit bureaus. Visit AnnualCreditReport.com to learn how.

Ways to improve your credit

Now that you know more about the benefits of good credit, you may want to work on improving yours. These seven steps for improving your credit could help:

- Check your credit scores often.

- Know some factors that go into a typical credit score.

- Keep an eye on your credit reports for errors.

- Learn how often you can check your credit reports.

- Understand which common credit card mistakes to avoid.

- Make payments on time and keep credit card balances low.

- Beware of quick credit score fixes.

Monitoring your credit regularly

Since credit can impact so many areas of your life, it can help to keep yours top of mind. And monitoring your credit regularly can help give you a big-picture view of your overall financial health.

CreditWise from Capital One is an easy way to monitor your credit score and credit report without hurting your credit scores. And it’s free for everyone, not just Capital One customers. You can also get free copies of your credit reports from each of the three major credit bureaus at AnnualCreditReport.com.