Does checking your credit score lower it?

If you’re worried that pulling your credit will lower your credit scores, don’t be. Checking your credit is a soft inquiry, which means it won’t cause your scores to drop. And actually, checking your credit reports and credit scores regularly can be a good idea.

If you monitor your credit, you could catch errors on your credit reports that might otherwise lower your credit scores. It could also help you spot potential fraud or identity theft.

What you’ll learn

- Checking your credit by using a soft inquiry won’t lower your credit scores.

- Hard inquiries, the type lenders use to review credit as part of loan applications, can cause a temporary dip in credit scores.

- Monitoring your credit regularly can help uncover errors and potential fraud or identity theft.

- Factors that affect credit scores include payment history, credit history and credit utilization.

How soft and hard credit inquiries impact your score

When it comes to credit reviews, there are two ways to request information:

- Hard inquiries

- Soft inquiries

Sometimes referred to as hard and soft pulls, the type of inquiry determines whether it will affect your credit scores.

Soft inquiries

Soft inquiries can appear on your credit report for up to two years, but they don’t affect your credit scores because they aren’t tied to lending.

Soft credit pulls are typically done by:

- Employers: to verify your credit

- Insurance companies: to give you policy quotes

- Credit monitoring companies: to check your activity

- Other companies: to promote a loan, insurance, credit card or credit limit increase

Hard inquiries

When a lender looks at your credit history to decide whether to lend you money or approve you for a credit card, that’s considered a hard inquiry or hard pull.

Hard pulls might temporarily lower your credit scores by as much as 10 points. But that drop will likely be temporary. They typically affect your credit scores for a year, but they can stay on your credit reports for up to two years.

Hard inquiries generally happen when you apply for:

- Credit cards

- Car loans

- Mortgages

- Personal loans or lines of credit

Because applying for a lot of credit in a short amount of time can negatively affect your credit, you might want to consider waiting between credit applications.

One exception is when you’re looking for the best interest rate on a mortgage or auto loan and multiple lenders check your credit around the same time. Credit bureaus will usually consider these mortgage or auto loan inquiries as one inquiry if they’re done in a short amount of time—typically 14 to 45 days. But multiple credit card applications will count as individual hard inquiries, even if they’re done on the same day.

Keep in mind, credit inquiries can also be done when you apply for things like a new apartment or utilities. So it’s a good idea to ask the person doing the credit pulls whether or not they could affect your credit.

How to check your credit score without hurting it

To check your credit score, you have a few options. You could use services through a lender or work with a credit counselor. Or you could monitor your credit with an app like CreditWise from Capital One.

CreditWise lets you access your credit report and credit score at any time. CreditWise is free for everyone—whether you have a Capital One card or not. And using it won’t hurt your credit scores.

If you want to check your credit reports, you can get free copies from each of the three major credit bureaus by visiting AnnualCreditReport.com.

Do I have to pay to check my credit score?

You can use paid services to check your credit score, but you don’t have to. Apps like CreditWise are free for everyone. And it gives you access to your credit score with a tap, so you can check whenever you like.

What affects your credit score?

A hard inquiry is just one of many things that can affect your credit scores. Collections, foreclosures and bankruptcies are some of the obvious derogatory marks on your credit reports that can also hurt your scores.

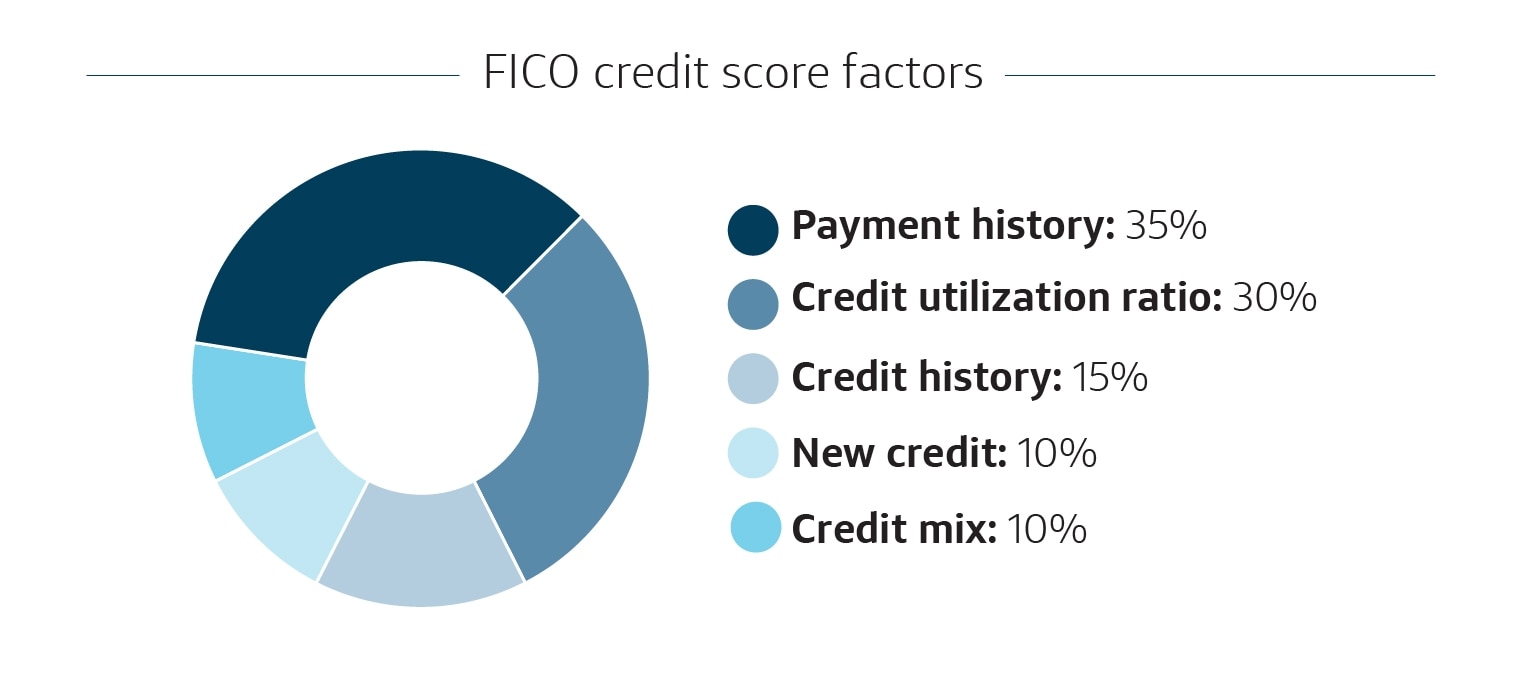

Knowing how credit-scoring companies calculate your scores may help you understand the less obvious reasons, though. Here’s a snapshot of the FICO® system and how much each of the following factors affects your credit scores:

- Payment history: 35% is based on whether you pay your bills and debts on time.

- Credit utilization ratio: 30% is based on the amount of debt you owe. That includes your credit utilization or the ratio between all of your credit balances and credit limits. If your credit utilization ratio is high, lenders could think you’ve already borrowed more than you can easily repay. So the Consumer Financial Protection Bureau recommends keeping this ratio at or below 30%.

- Credit history: 15% is based on how long you’ve had credit accounts, how long each account has been open and how long it’s been since you used each one. Basically, the longer, the better.

- New credit: 10% is based on how many accounts you’ve opened or applied for recently. Lenders may consider it risky if you’ve applied for too much credit in a short amount of time.

- Credit mix: 10% is based on the different types of credit you have. Lenders favor diversity, so it could be good to have an array of credit, such as a mortgage and a credit card—as long as you pay them on time.

How to improve your credit score

Here are some things that can help your credit scores:

- Monitor your credit. This can give you an idea of where your credit stands and let you look out for any errors on your credit reports. You can visit AnnualCreditReport.com to get free copies of your credit reports or use a free credit monitoring tool like CreditWise.

- Pay your bills on time. Because payment history is a major factor in calculating your credit scores, it’s always a good idea to pay your bills on time. Setting up reminders or automatic payments can help.

- Keep your credit utilization ratio below 30%. One way to help lower your credit utilization ratio is by paying more than the minimum amount due for your credit accounts.

- Consider a secured credit card. If you’re having trouble getting approved for credit, you might want to think about applying for a secured credit card. Getting a secured credit card involves paying a refundable security deposit.

- Only apply for the credit you need. That way, you can limit hard credit inquiries, which can negatively affect your credit scores.

Key takeaways: Does checking your credit score lower it?

Reviewing your credit reports and credit scores can be a good way to see where your credit stands—and uncover any errors or signs of potential fraud and identity theft. Remember, a soft inquiry into your own credit history won't lower your credit scores. But hard inquiries can cause your scores to drop temporarily.

Keeping an eye on your credit score can help you know where you stand before you apply for loans or new lines of credit. If you’re looking for a free and easy way to keep tabs on your score, CreditWise may be a good option. It’s available to everyone, even if you’re not a Capital One cardholder.