What’s the highest credit score possible?

If you’ve ever wondered what the highest credit score you can have is, it’s 850. That’s at the top end of the most common FICO® and VantageScore® credit scores. And these two companies provide some of the most popular credit-scoring models in America.

But do you need a perfect credit score? Not necessarily. According to research by credit bureau Experian®, a score above 760 could qualify you for the best interest rates.

Read on to learn more.

Key takeaways

- Generally speaking, the highest credit score possible is 850, according to the most common FICO and VantageScore credit models.

- There are several factors that go into determining a credit score, such as payment history, amounts owed, length of credit history, credit inquiries and credit mix.

- A higher credit score can help you qualify for credit—from mortgages to credit cards—with more favorable interest rates.

- Building healthy credit habits like paying bills on time and keeping credit utilization low can help you establish and maintain good credit scores.

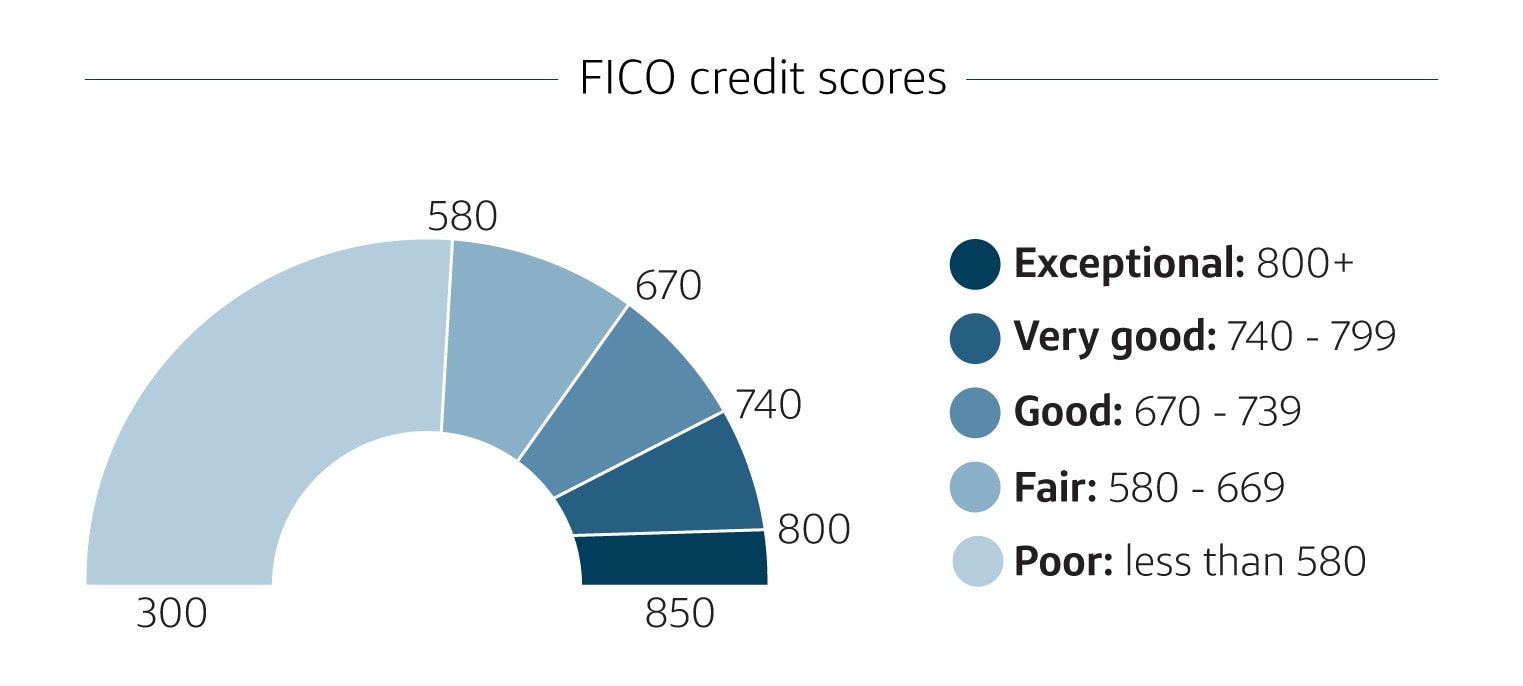

Understanding credit score ranges

Sure, you want to achieve a high credit score. But how do you know when your credit score moves from the “good” to “excellent” range?

Not all scoring models are the same. But most label a range of scores from “poor” to “excellent” as a way to show how a lender might view them. FICO breaks its scores down like this:

Source: MyFICO.com

Who determines credit scores?

Credit-scoring companies use the information from your credit reports to calculate your credit scores. Two companies—FICO and VantageScore—provide some of the most popular credit-scoring models in America. Most of their models top out at a score of 850.

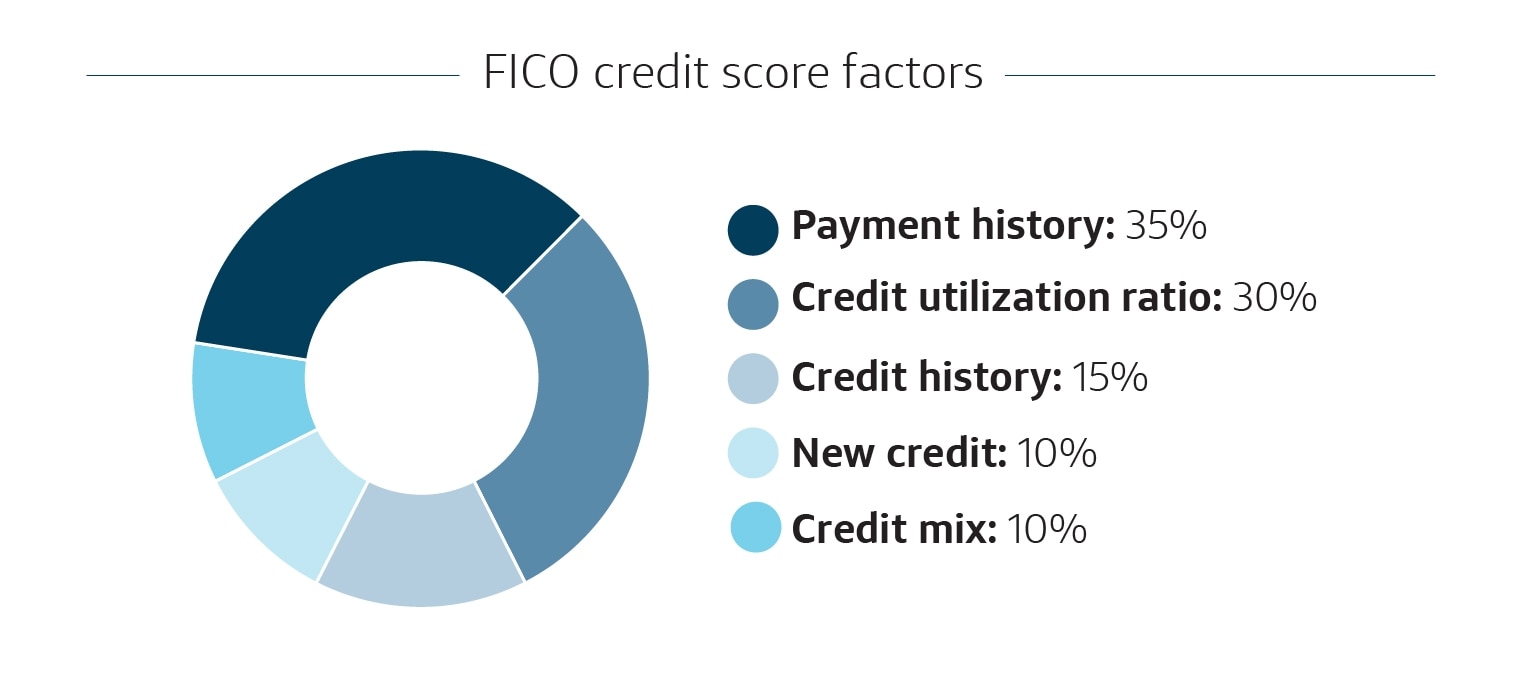

What factors affect credit scores?

There are a few different factors that affect your credit scores. And how they affect your scores depends on the credit-scoring model and the company doing the scoring.

Here’s how FICO groups and weighs the different credit factors:

- Payment history: 35%

- Amounts owed, including credit utilization: 30%

- Length of credit history: 15%

- New credit inquiries: 10%

- Credit mix: 10%

Source: MyFICO.com

What are the advantages of having an excellent credit score?

Generally speaking, higher scores indicate that you’re more likely to repay your debts and manage credit responsibly.

With high credit scores, you might:

- Qualify for lower interest rates. According to the Consumer Financial Protection Bureau, lenders typically offer the lowest interest rates to those with the highest credit scores.

- Get approved for a higher amount. You may be able to get a higher limit on your credit card or a bigger loan.

- Have more housing choices. Higher credit could make it easier to rent an apartment or get a mortgage.

- Find it easier to get utility services. According to the Federal Trade Commission, the better your credit history, the easier it’ll be to get utility services.

- Have an easier time getting a cellphone. With good credit, you may be less likely to have to prepay or put down a security deposit when opening a cellphone account.

- Qualify for potential jobs. Some companies might look at your credit reports as part of their background checks.

- Pay lower insurance premiums. Some insurance companies use your credit reports to help them decide whether to approve insurance applications and how much to charge in premiums.

How to get a perfect credit score

In 2019, FICO released research about the habits of U.S. consumers who reached scores of 800 or greater using its FICO Score 8 model. According to that study, people who maintained high credit scores followed a similar pattern.

Some of the habits these people practiced included:

- Paying their bills on time. About 96% of those with an 800-plus FICO score pay their credit accounts on time.

- Keeping their credit use to a minimum and keeping low balances on credit cards. FICO says that people with 800-plus FICO score ratings usually only use about 7% of their available credit, which is known as their credit utilization ratio.

- Avoiding credit checks. You probably can’t avoid a hard inquiry here and there, but “overapplying” within a short period of time might hurt your score.

- Keeping old accounts open. Those with high FICO scores have accounts open for an average of 11 years. Just remember that keeping an account open may not be enough since it could eventually be closed due to inactivity. Be sure to contact your lender for details.

How to monitor your credit score

Monitoring your credit is important when trying to maintain or improve your credit scores. It can help you see exactly where you stand—and how much progress you’ve made.

One way to monitor your credit is with CreditWise from Capital One. CreditWise gives you access to your credit report and credit score anytime. And using it won’t hurt your scores. You can even explore the potential impact of your financial decisions before you make them with the CreditWise Simulator.

CreditWise is free and available to everyone—even if you’re not a Capital One cardholder.

You can also get free copies of your credit reports from all three major credit bureaus—Equifax®, Experian® and TransUnion. Call 877-322-8228 or visit AnnualCreditReport.com to learn more.

High credit scores in a nutshell

A perfect credit score is generally considered to be 850. And that’s a great goal to aim for. But Experian notes that “lenders don’t typically distinguish between scores that are in the ‘exceptional’ range of 800 to 850.” That means you’re unlikely to get any more benefits even if you do have a perfect credit score—though it’s a worthy goal to strive for.