What is a credit card balance?

Understanding the difference between each type of balance on a credit card can be confusing at first. But knowing which balance you’re responsible for paying each billing cycle could help you better manage your card. It could also help you pay less in credit card interest, fees and other penalties.

Here’s a breakdown of what credit card balances are, where to find them and some ways to manage them.

What you’ll learn:

-

A credit card balance is how much money you owe your credit card issuer.

-

Making purchases with your card will increase your balance, while making payments will decrease it. Other factors like interest and fees may also impact your credit card balances.

-

A statement balance shows the amount you owe your issuer at the end of each billing cycle. A current balance changes as you make new purchases and payments.

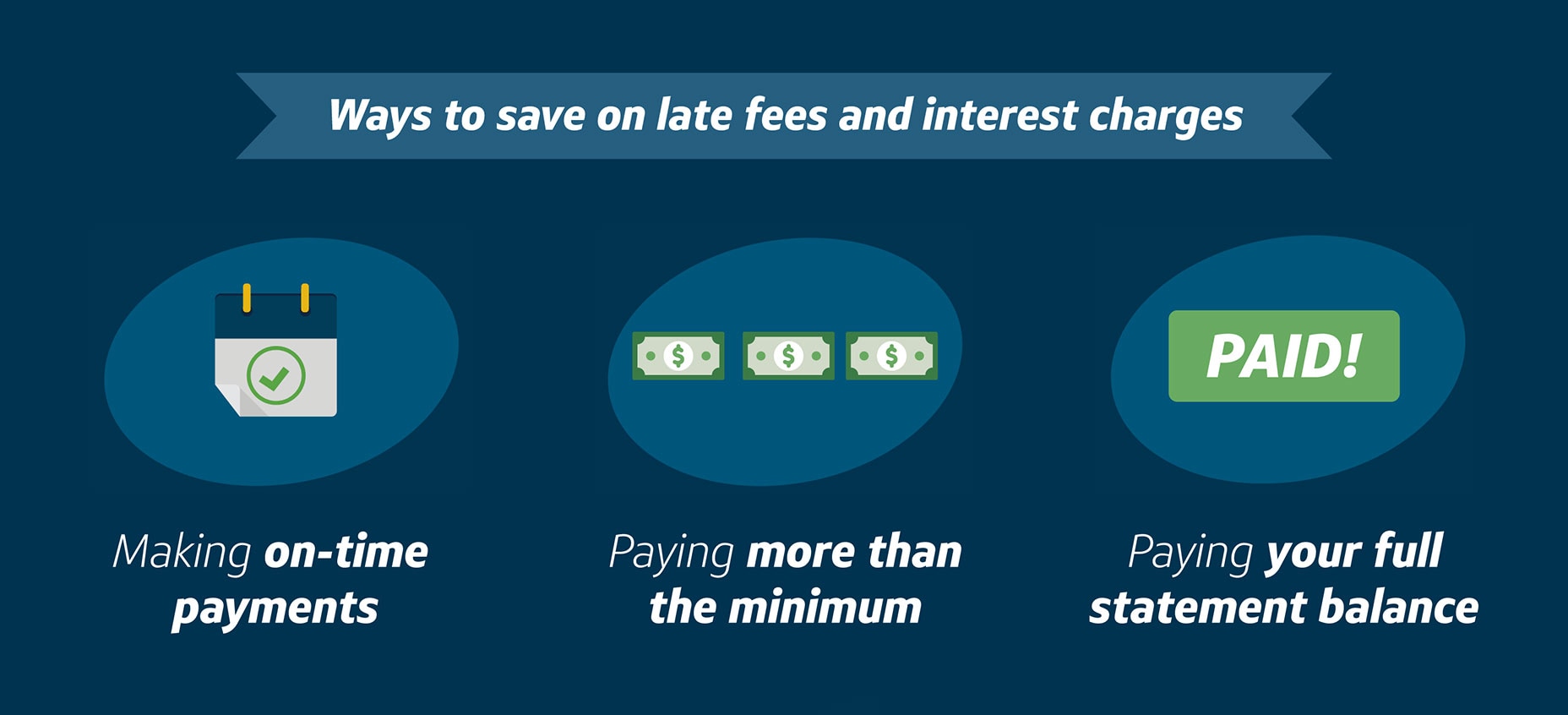

- Paying off your statement balance by the due date each month could help you avoid interest charges. And making at least the minimum payment by your due date could help you avoid late fees and other penalties.

What does credit card balance mean?

Your credit card balance is the total amount of money you owe your credit card issuer. That amount may include purchases and other transactions made with the card, plus interest and fees.

How are credit card balances calculated

Many factors can influence credit card balances, including:

As credit card payments are made, the total balance decreases. Paying off the entire balance each billing cycle can help you avoid interest charges altogether. Late or missed payments may lead to fees, interest charges and other penalties. Making at least the minimum payment on time can help you avoid these fees and penalties, but interest may still be charged on any remaining account balance.

What’s the difference between statement balance and current balance?

Your credit card statement will likely show a few balances, along with a minimum monthly payment. Knowing the difference between each type of balance could help simplify card management.

Here’s a breakdown of common balances:

Statement balance

A statement balance, sometimes called a new balance, shows how much you owe at the end of each billing cycle, which is typically 20-45 days. It’s the total of all purchases, fees, interest and unpaid balances minus any payments or credits.

Current balance

A current balance is a snapshot of the amount you owe at the time you check it. Like a statement balance, a current balance also captures the total of all your purchases, fees, interest and unpaid balances minus any payments or credits. But the current balance may fluctuate throughout the billing cycle as you make new charges and payments.

Minimum monthly payment

The minimum monthly payment is the amount your card issuer requires you to pay by the due date. Making at least the minimum payment on time helps keep your account in good standing. It can also help you avoid late fees and derogatory marks on your credit reports. However, interest might be charged on the unpaid portion of your statement balance. One way to avoid or reduce interest is to pay off your entire statement balance every month.

How do you check your credit card balance?

You may be able to check your credit card balance by using your issuer’s mobile app, signing in to your online account or reviewing your paper statements.

Regularly checking your balances can help you understand exactly how much you owe. Just remember that your statement balance and current balance could be different, depending on when you check your statement.

Another benefit? Reviewing your balances could also make it easier to spot unusual activity on your account.

Should you carry a balance on your credit card?

The Consumer Financial Protection Bureau (CFPB) recommends paying as much as possible toward your statement balance each month. Doing this can help you pay off your credit card debt more quickly and help limit the interest you’ll owe over time. The less interest you’re charged, the lower your future card payments could be.

What if I have a negative balance?

A negative balance on your credit card statement indicates that your card issuer owes you money. For example, this can happen after returning an item that results in a refund, overpaying your balance or receiving cash back as a statement credit from a cash back credit card.

Does a high credit card balance affect your credit score?

Carrying a high credit card balance isn’t just costly. It can affect your credit scores, too.

That’s because credit-scoring companies use your credit utilization ratio when they calculate credit scores. Your credit utilization ratio is a measure of how much of your available credit you’re using across all your revolving credit accounts.

A high credit card balance could negatively impact your credit utilization ratio. And a high credit utilization ratio could negatively impact your credit scores. That’s why the CFPB recommends keeping your credit utilization ratio below 30%.

How to manage high credit card balances

There are strategies that can help manage high credit card balances and other debts. They include:

-

Contacting lenders: The CFPB and the Federal Trade Commission recommend contacting individual lenders to investigate your options. Even small changes, like requesting a new due date, might make it easier to keep up with payments.

-

Applying for a balance transfer credit card: A balance transfer lets you move one or more of your credit card balances to a card from a new issuer. Some balance transfer credit cards come with a low or 0% introductory APR offer. If your transferred debt is paid off by the end of the card’s introductory period, you could save on interest. Keep in mind that you may have to pay a balance transfer fee.

- Taking out a debt consolidation loan: This type of personal loan can be used to pay off credit card debt and other types of debt. Like a balance transfer, a debt consolidation loan can also be a useful tool for combining multiple debts into a single monthly payment. And if the loan has a lower interest rate, you may be able to pay off your debt faster.

Key takeaways: What is a credit card balance?

Understanding how credit card balances work can help you as you manage your finances. And by checking your balance regularly, you’ll know how much available credit you have and how much you may owe at the end of each billing cycle.

Now that you know more about credit card balances, you may want to compare Capital One cards that might fit your needs. And with pre-approval from Capital One, you can find out whether you’re pre-approved before applying. It’s quick and it won’t hurt your credit score.