How to calculate APR on money you borrow

If you’re shopping for a loan or credit card, you may notice something called the annual percentage rate (APR). APR represents the annual cost to borrow money. To calculate APR, you’ll need some basic information about your loan, like total interest charges, fees, loan amount and number of days in the loan term.

Knowing about APR can help you compare credit offers and find the one that’s best for you. But different factors—like the loan type or your creditworthiness—can influence the APR you’re offered.

What you’ll learn:

-

APR represents the annual cost of borrowing money, shown as a percentage.

-

The formula to calculate APR is: APR = (((Interest + Fees ÷ Loan amount) ÷ Number of days in loan term) x 365) x 100.

-

APRs may be higher than interest rates because they include the interest rate plus other costs, such as lender fees. But when it comes to credit cards, the APR and interest rate are typically the same.

- Some credit card issuers offer temporary promotional rates, such as 0% introductory APRs.

What is APR?

APR is the yearly cost of borrowing money. Understanding APR can give you a better picture of borrowing costs than interest rates alone.

While interest rates and APRs both represent the cost of borrowing money, they’re not exactly the same. The main difference between APR and interest is that the interest rate is the amount the lender charges to borrow the principal balance, while APR represents the interest rate plus any other fees related to the loan.

Types of APR

Most credit card accounts have a variable APR. But it’s still helpful to know the difference between variable and fixed APRs.

-

Variable APR: These may be determined using a benchmark interest rate, such as the prime rate. A variable APR can change as the benchmark interest rate goes up or down.

- Fixed APR: Fixed APRs aren’t tied to an index rate, meaning they won’t change the same way. They’re sometimes referred to as non-variable APRs, but that doesn’t mean they never change.

APR formula

You can calculate APR using this formula:

APR = (((Interest + Fees ÷ Loan amount) ÷ Number of days in loan term) x 365) x 100.

The APR formula involves a few important factors: the total interest charges, fees, loan amount and number of days in the loan term. Here’s what each means.

-

Interest charges: This charge is the total cost of borrowing money. Lenders should tell you the interest rate when you receive a loan offer. You could also find it in your loan agreement, or if you’ve already taken out a loan, it should be listed on your statements.

-

Fees: These can vary by loan type and lender. Review your terms and conditions to find the fees that could apply to your loan.

-

Loan amount: You’ll need to know the original loan amount, also called the principal.

-

Days in the loan term: Since APR measures the annual cost of borrowing money, multiply 365 by the number of years in the loan’s term. For terms that are less than one year, use the number of days.

The Truth in Lending Act requires lenders to disclose APR when they offer you credit. You could also use an online calculator to estimate a loan’s APR.

How to calculate APR on a loan in 7 steps

While you might not use the APR formula on a regular basis, it could be helpful when you compare loan offers.

Here’s an example of how to calculate the APR of a $5,000 personal loan with a 5% origination fee, 10% interest rate and 3-year repayment term.

1. Find the interest rate and charges

For the APR formula, you’ll need to determine a loan’s total interest charges. If the loan charges simple interest, you could use the simple interest method. To do this, multiply the principal by the interest rate and the number of years in the repayment term.

2. Add the fees

Next, add the loan’s finance charges or fees to the interest charges. In this case, the 5% origination fee is $250 because 0.05 × 5,000 = 250.

3. Divide the sum by the principal balance

Once you know the sum of your interest charges and fees, divide that number by your original principal balance.

4. Divide by the number of days in the loan’s term

Divide the last result by the number of days in the loan’s term. With a 3-year loan, that would be 1,095 days.

5. Multiply by 365

Now, multiply that number by 365 to get the annual rate.

6. Multiply by 100

Finally, multiply the previous number by 100 to get the annual rate as a percentage.

7. Learn your APR

For this example, the loan’s APR would be 11.67%.

How do you calculate APR on a credit card?

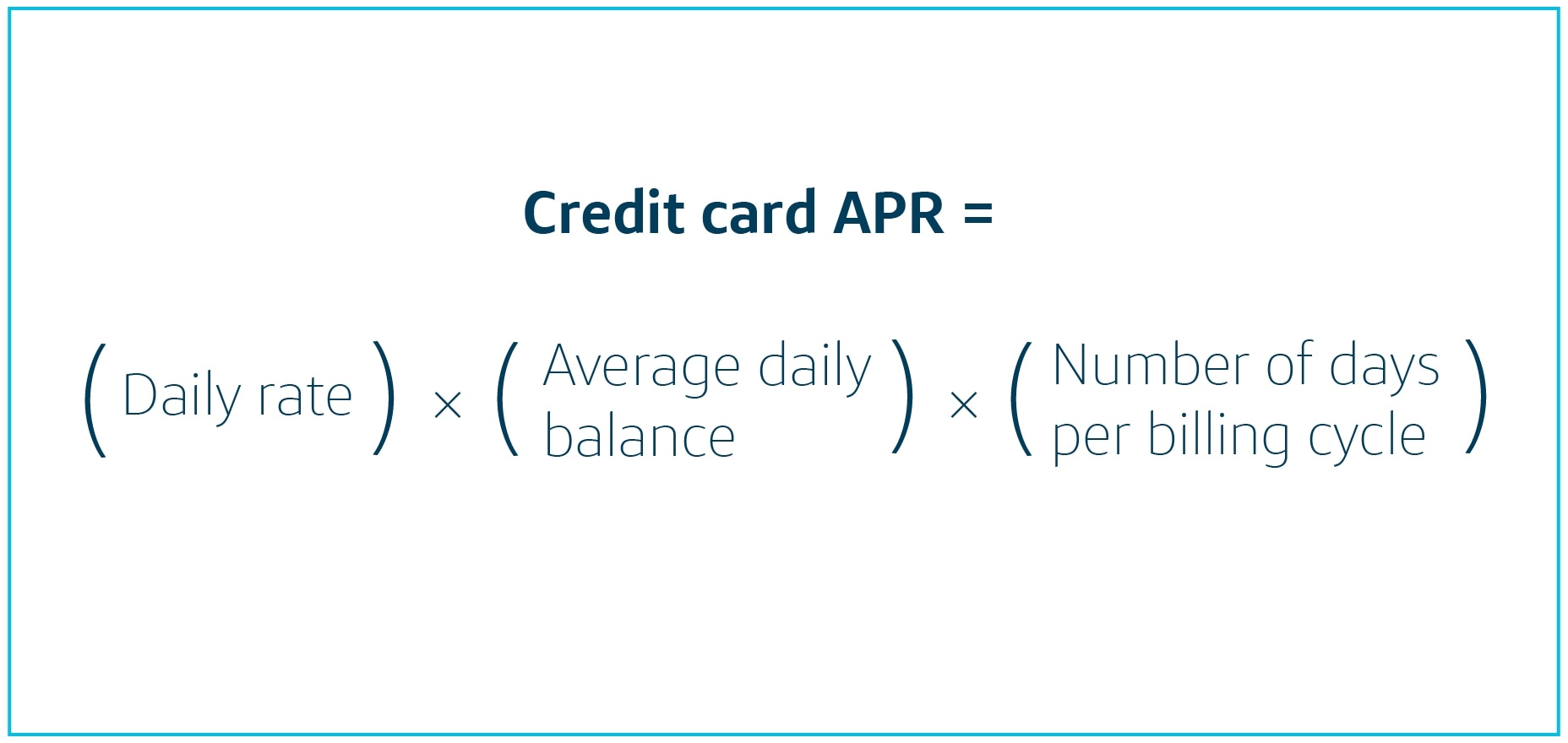

You can calculate the APR that’s applied to your credit card balance within a billing cycle by multiplying your daily rate by the average daily balance and by the number of days per billing cycle. You’ll just need to find those numbers first.

-

Daily rate: You can determine the daily rate by dividing the APR by 365. If your card has a 22% APR, your daily rate would be 0.06%. Use the decimal form when you plug this rate into the formula.

-

Average daily balance: Total the credit card balance from each day in the billing cycle. Then, divide it by the number of days in the billing cycle to find the average daily balance.

-

Number of days per billing cycle: Credit cards typically have a billing cycle that’s 28 to 31 days. You can review your loan agreement or statements to find the number of days in your card’s billing cycle.

Once you find these numbers, you can plug them into the credit card APR formula.

Credit card APR formula and example

The formula to calculate credit card APR is:

Credit card APR = Daily rate × Average daily balance × Number of days per billing cycle

For example, a cardholder with a daily rate of 0.06%, a daily balance of $100 and a 28-day billing cycle would owe the following in APR:

0.0006 × $100 × 28 = $1.68

So if these were the terms and balance of your credit card, you would pay $1.68 in monthly interest.

But keep in mind that if you pay off your balance every month before the due date, you usually won’t have to pay any interest on new purchases.

How is credit card APR determined?

The credit card issuer determines a credit card’s APR, which is usually the same as the card’s interest rate. Keep in mind, issuers are required to notify you of changes to your APR or an increase in your minimum monthly payment.

Some factors issuers use to determine APR include:

-

Credit scores: Card issuers may use your credit scores to determine interest rates. So when an issuer determines the APR for a credit card, your credit history could influence the rate you’re offered.

-

Type of purchases: Different types of transactions could have different APRs. So it’s wise to review the terms in your loan agreement to find out. For instance, a credit card issuer may charge one APR for regular purchases, one for balance transfers and another for cash advances.

- Introductory offers: There are other factors that can also affect your credit card APR. Some credit cards have introductory offers, such as 0% APR. Once that promotional period ends, the APR could increase.

APR vs. APY

APR might sound similar to annual percentage yield (APY). But APR measures the annual cost of borrowing money, while APY is the amount earned on things like savings accounts or certificates of deposit.

It’s also important to note that APR calculations don’t include compound interest like APY does. Reviewing your loan terms or monthly statements may help you better understand your total borrowing costs.

Key takeaways: How to calculate APR

Calculating APR on a loan or credit card can help you understand how much it might cost you to borrow money. Since APRs are a broader measure of borrowing costs than interest rates, it can be helpful to compare APRs when you shop for loans or apply for credit cards.

The interest rate and APR are typically the same for credit cards, but some credit cards may offer promotional APRs. If you’re looking for a new card, you could compare Capital One credit cards to see which card best matches your needs.