The debt snowball method: What it is and how it works

If you’re one of countless Americans wondering how to pay off debt, you’ll probably be relieved to hear that there’s more than one way to do it. And one of those ways is the snowball method.

You might be asking, “What is the snowball method?” Learn how it compares to other debt repayment strategies and how it could help you get closer to becoming debt free.

Key takeaways

- When paying off debt using the snowball method, you start by paying off debts with the lowest balances.

- From there, the money that’s freed up by eliminating those smaller debts can snowball and eventually be put toward larger and larger balances.

- The debt snowball method can help provide structure to debt repayments, but you may end up paying more in interest if larger debts also have higher interest rates.

- If it makes more sense to eliminate high-interest debt first, the debt avalanche method is another strategy that might be worth exploring.

What is the debt snowball method?

The debt snowball method is a strategy that focuses on repaying outstanding debt with the smallest balance first. After paying off the smallest debt, that extra money can be put toward paying off your next smallest debt and so on. The idea is that your money can gradually snowball and eventually help you pay off larger and larger balances.

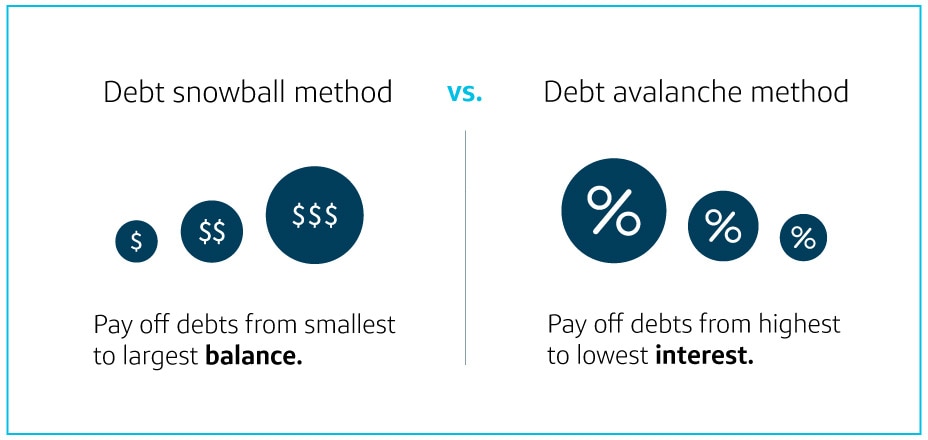

Debt snowball vs. debt avalanche

The debt avalanche method is another common debt repayment method that’s often compared to the debt snowball strategy.

With a debt avalanche strategy, you focus on paying off debt with the highest interest rate first. Once that debt is paid off, you can put the extra money from those payments toward payments on other lower-interest debt.

Repaying debt using the avalanche method might take longer than the debt snowball method. But the avalanche method might result in paying less overall in interest.

How does the debt snowball method work?

The debt snowball method focuses on small victories. This is accomplished by paying off your smallest debt first, then your next-smallest debt and so on until you’re debt free.

Here are some suggestions that can help get you started with the snowball method:

1. Make a list of debts

Create a spreadsheet or get a notepad and write down each outstanding debt. This can include credit cards, student loans, medical bills and any other types of debt you have. Include information like the full amount you owe, the minimum monthly payment, the interest rate and the monthly due date, just to stay on track.

2. Continue to make on-time payments

You’ll want to continue making the minimum monthly payment on all your debts while using the debt snowball method. Payment history makes up 35% of your total credit score. So the more on-time payments you make, the fewer fees you’ll be charged and the more positive impact the payments can have on your credit score.

3. Focus on paying off the smallest debt

While you make minimum payments on the rest of your debts, put any extra funds available toward your smallest debt.

If you’re looking for ways to find extra income to help with this, consider ways you can make extra money, like a side hustle. Wherever extra income comes from, you can put it toward that smallest debt.

4. Repeat until complete

Continue putting all your extra cash toward that smallest debt until it’s paid off. Then you can apply the money you were paying on that debt to your next-smallest debt. Do this until all your outstanding debts are paid in full.

The debt snowball method in action

Wondering how this might actually work? Here’s an example of what the snowball method could look like in action:

| Account type | Minumum monthly payment | Interest rate | Balance |

| Medical bill | $125 | 0% | $1,500 |

| Credit card A | $100 | 24% | $3,000 |

| Credit card B | $130 | 16% | $4,000 |

| Car loan | $218 | 3% | $7,500 |

| Student loan | $122 | 4% | $10,000 |

| Total minimum due | $695 |

In this example, the medical bill is the smallest debt. So with the snowball method, you put any extra money you have available toward that bill.

At the same time, you’ll continue to make the minimum monthly payments on all the other debts.

Once the medical bill is paid off, you can focus on the next-smallest bill, credit card A. Roll the funds you were using to pay the medical bill—and any other extra cash you might have—into paying off that bill next.

Once the medical bill and credit card A are paid off, the process is repeated with credit card B, the car loan and then the student loan. The amount you can pay on each bill will continue to snowball until you have all your debts paid off.

Pros and cons of the snowball method

There are some potential benefits and drawbacks to using the debt snowball method.

Pros

The debt snowball method can be good for people who like to see progress quickly as they pay off smaller debts. It can help make your debt repayments feel a little more manageable, because you’re gradually building momentum and working your way toward larger balances over time. And it may help you feel more motivated to keep going by seeing small wins earlier on in the debt repayment process.

Cons

Snowballing your debt may not always be the most cost-efficient strategy. That’s because the debt snowball method focuses on the smallest debt first, regardless of the total amount of debt owed or what interest rate you’re paying. And the higher the interest rate, the more you’ll pay over the life of the loan. So if you have a lot of outstanding credit card debt or large amounts of debt, this might not be the right plan for you.

Other ways to reduce debt

The debt snowball method is one way to pay off debt, but it’s not the only way. There are other options to choose from.

Debt consolidation

If you have a lot of different types of debt, you might want to try debt consolidation. This is when you combine multiple debts, then make a single payment toward your loan or line of credit. This can help streamline your debt, giving you one due date and payment instead of many.

This may be a good option if you can get an interest rate lower than what you’re paying now. Otherwise, it might not be worth consolidating. Instead, you might want to explore other cost-saving options.

Credit card balance transfer

Carrying a balance on your credit cards can cause interest charges to add up. In this situation, if you want to avoid high interest charges, you might consider a balance transfer. This lets you move unpaid debt from one or more accounts to a new or different credit card. It can help you consolidate debt or get a lower interest rate, which could help you pay off your debt faster.

Just be sure to review all the terms and conditions before applying. Especially since there may be fees associated with a balance transfer. Plus, you’ll want to check what interest rate you could be charged once the introductory rate ends. And keep in mind how canceling any old cards might affect your credit score.

Talk to the lender or a credit counselor

For those struggling to pay bills on time or repay outstanding debts, it may help to contact your lender about what options are available. A credit counseling service might also be able to help. A reputable counselor might be able to provide everything from personalized budgets to general education classes. Some counselors might even be able to organize debt management plans to help people pay down debts.

The debt snowball method in a nutshell

If you’re looking to quickly pay down your smallest debts first, the snowball method may be a good place to start. But consider different debt payoff strategies until you find the one that works for you.

Just remember, there are several ways to pay off debt. Consider your unique financial situation and the different types of debt you have to help you choose which approach to take.