Loan-to-value (LTV) ratio: What you need to know

When you apply for a secured loan, the lender may calculate the loan-to-value (LTV) ratio and use it to help make an informed lending decision. The LTV ratio compares the loan amount with the value of the asset you’re buying, such as a home, and it’s often expressed as a percentage.

Along with your creditworthiness, income and debt-to-income ratio, a loan’s LTV ratio could be an important factor in loan approvals and terms.

Key takeaways

- Loan-to-value ratios are used to measure how a loan amount compares to the asset it’s being used to purchase.

- Loan-to-value ratios change as payments are made, assets increase in value or both events occur.

- Lenders may use loan-to-value ratios to inform lending decisions.

- The lower the loan-to-value ratio, the less risky it may be for lenders.

- Lower-risk loans may be easier to be approved for.

What a loan-to-value ratio means when purchasing real estate

The LTV ratio on a mortgage can be especially important because, along with impacting the approval and terms of your loan, you may need to purchase mortgage insurance if you have less than 20% equity in the home. Or, looking at it another way, the insurance may come into play if your LTV is over 80%.

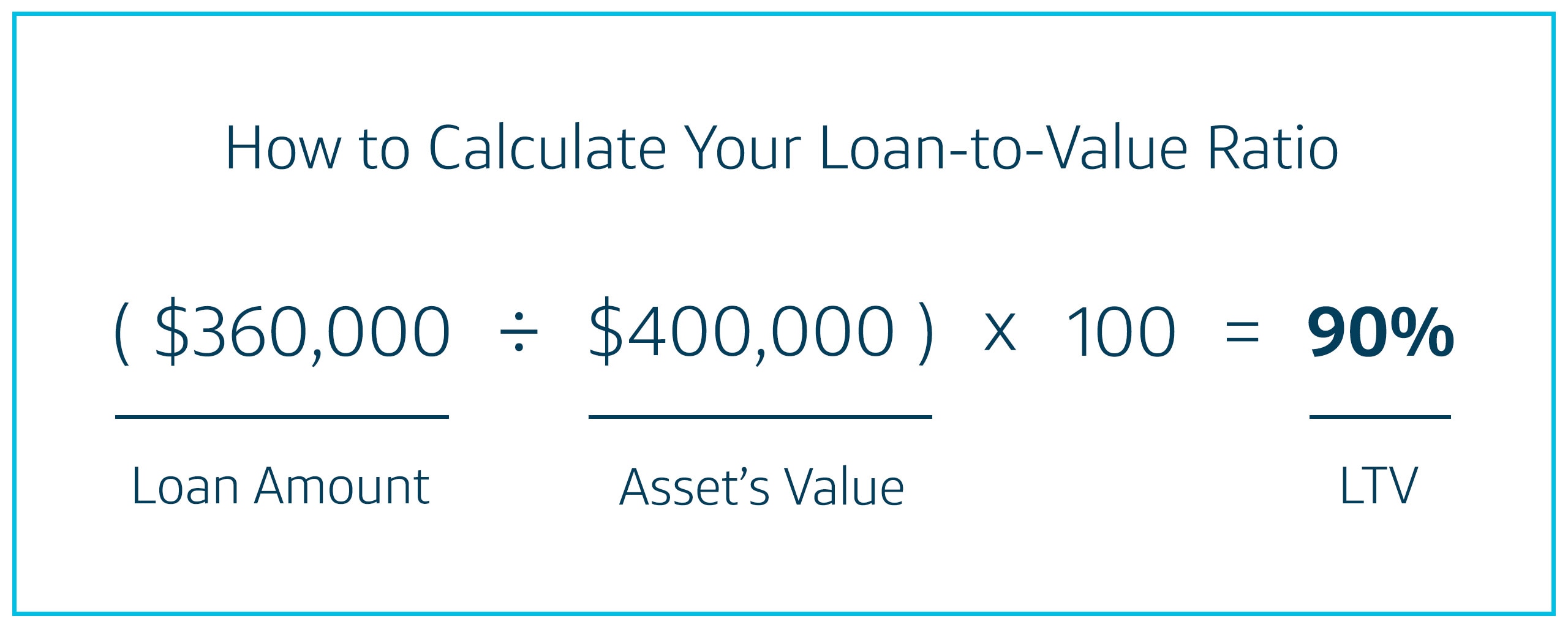

Loan-to-value ratio formula and LTV example

The LTV ratio formula is fairly straightforward, as it only involves the loan amount and the value of the asset you’re buying.

For example, with a mortgage, the LTV ratio is the loan amount divided by the home’s appraised value. If you put 10% down ($40,000) and buy a $400,000 home, your mortgage will be $360,000. To find the LTV ratio, if you divide 360,000 by 400,000, you will get 0.90. To get the ratio as a percentage, multiply 0.9 by 100, which is 90%.

Because your LTV ratio is over 80%, you may need to pay for private mortgage insurance (PMI), a policy that helps protect mortgage lenders. As a homeowner, you may also need a separate home insurance policy, which is what protects you. But paying a high down payment could reduce the LTV ratio and help you avoid paying PMI.

Your equity and LTV ratio change as you pay down the mortgage and as the value of your home increases or decreases. Once your LTV ratio drops below 80%, borrowers may be able to request to remove the PMI. But some mortgage lenders may require borrowers to wait until they have at least 20% equity based on the home’s original appraised value rather than its current value.

How lenders use LTV ratios

A loan’s LTV ratio is one factor lenders might use to help make decisions about loan applications, rates and terms. A higher LTV ratio is riskier for lenders. More of their money is on the line, and the borrower may be less invested (literally and figuratively) in keeping up with their payments.

Consider someone who buys a $400,000 home with 5% ($20,000) down, an LTV of 95%. If the housing market drops, this person might have a $380,000 mortgage for a home that’s now worth $350,000—they’re “underwater” on the loan. They may decide that their best course of action is to stop making payments and let the home go into foreclosure, even if it will hurt their credit.

If the lender had required a larger down payment, which resulted in a lower LTV, the borrower might have more money at stake and be less inclined to walk away from the home.

Loan-to-value ratio rules and variations

You may be able to choose from different types of mortgages when you’re trying to buy a home. The maximum allowed LTV—and minimum down payment—can vary depending on the type of mortgage.

FHA loans

Federal Housing Administration (FHA) loans may have a maximum LTV of 96.5%. These loans also require a mortgage insurance premium (MIP), which you might have to continue paying even after your equity is above 20%. If your LTV ratio was over 90% when you took out an FHA loan after June 2013, you may not be able to remove the MIP at all.

USDA and VA loans

Many government-backed U.S. Department of Agriculture and Department of Veterans Affairs home loans don’t require a down payment, which means your LTV ratio could be as high as 100%.

Conventional loans

Conventional mortgage loans—mortgages that aren’t backed by a government program—may require a lower LTV ratio. If you want a conventional loan without having to pay mortgage insurance, you may need to put at least 20% down and have an LTV of 80% or lower. There are also conventional loans with a maximum LTV of 95% to 97%, but they may require PMI.

Loan-to-value (LTV) ratio vs. combined loan-to-value (CLTV) ratio

While your LTV ratio only looks at the amount of your loan and the value of the collateral, the combined loan-to-value (CLTV) ratio includes additional loans that you take out against the asset.

If you only have one loan, your LTV and CLTV will be the same.

But after you buy a home, you may want to take out a second mortgage, such as a home equity loan (HEL) or home equity line of credit (HELOC). The CLTV could then include:

- The current balance on your first mortgage.

- The current balances on any additional home equity loans.

- The amount you’ve borrowed against home equity lines of credit.

The sum of these amounts is then divided by the home’s value to determine the CLTV. In some cases, lenders may also look at your home-equity-combined-loan-to-value (HCLTV) ratio, which will include the entire approved amount of HELOCs rather than the amount you’ve borrowed.

Your CLTV and HCLTV can impact your ability to get an HEL or HELOC, along with the maximum loan or credit limit amounts and the loans’ interest rates.

FAQ about loan-to-value ratios

What’s a good LTV ratio?

When you’re buying a home, a good LTV ratio is 80% or lower. If you can put at least 20% down, you may be able to avoid paying for mortgage insurance and potentially get a lower interest rate on your loan, both of which can lower your monthly payment.

Are there disadvantages to having a high LTV ratio?

You may find it hard to get approved for a loan that has a high LTV ratio. Even if you do get approved, a higher LTV ratio can lead to a higher interest rate or having to buy mortgage insurance.

Is there a way to lower your LTV ratio?

You can lower your LTV ratio by making a larger down payment or taking out a smaller loan. This may mean buying a smaller home or buying in a less-expensive area. Once you’ve gotten a loan, you can lower the LTV ratio by making loan payments, and the LTV will rise or fall based on your home’s changing value.

Key takeaways: Loan-to-value ratio

A loan’s LTV ratio is a comparison of a secured loan’s balance to the collateral’s value. It’s one of the many factors that lenders use to determine how risky a loan is and how much they’ll charge you to borrow money. Generally, the lower the loan’s LTV ratio, the easier and cheaper the lower the loan’s LTV ratio will be, making it easier to get a loan.

Lenders also look at various other factors, such as your credit history and credit scores. You can sign up for CreditWise from Capital One to check your credit report and credit score. You can also receive ongoing free credit monitoring and alerts.