Professionals expecting innovative mobile solutions

Commercial card customers continue to anticipate the introduction of the next generation of card innovations from their providers.

Raj Dutt

Capital One Head of Product Strategy, Commercial Card

This article first appeared in Payments Journal on August 23, 2018.

Commercial card customers continue to anticipate the introduction of the next generation of card innovations from their providers. That’s the conclusion gleaned from Capital One’s most recent survey of corporate card end-users, which it conducts each April at the NAPCP Commercial Card & Payment Conference.

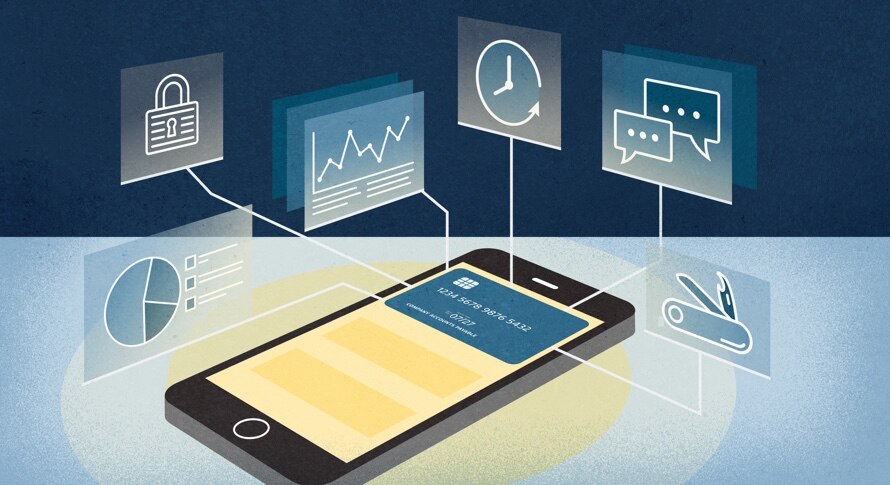

Mobile: The promise of 24/7 convenience and control

Where will providers be concentrating their creative energies? One answer, clearly, is mobile. The benefits of mobile apps for both cardholders and administrators are abundant.

For cardholders, mobile apps that can serve up real-time balances and credit availability help to keep spending on track. In addition to alerting cardholders of approaching credit limits, some mobile apps can even send travel notifications to banks to ensure their transactions are approved.

Mobile apps also provide a range of options that can reduce the pain of documenting T&E expenses. For example, with their smartphone in hand, cardholders can scan receipts into the app, allowing for app integration with location services to make mileage entries automatic. Finally, mobile apps could make it easier for cardholders to play a more active role in managing their accounts, for instance entering a new address when they move or requesting increases in their credit limits.

From the administrators’ perspective, mobile apps could also have a number of compelling advantages. They have the potential to free administrators from their desks, providing a 24/7 window on important commercial card activity throughout their organization and giving them the opportunity to address key issues and concerns as they arise. Mobile access has the power to enable administrators to dispute debits immediately, adjust cardholder access, and revise permissions in real-time. In addition, mobile apps allow administers to spend more time on strategic issues by transferring certain routine card maintenance actions to cardholders.

Flawed design and implementation puts mobile adoption on hold

Given these potentially powerful advantages, it’s surprising that mobile commercial card apps have not gained more traction with commercial card customers. Eighty-seven percent of the respondents to Capital One’s survey reported that their providers offer a mobile app. Professionals, however, have been slower to adopt. According to the survey, however, 53 percent of the professionals polled said their organizations do not use mobile apps to view or manage commercial card transactions or remotely submit travel expenses.

A closer look at the results of the Capital One survey suggests that flawed implementation might be to blame. Twenty-five percent of the organizations that use a mobile app for either commercial transactions or travel expenses prefer to use their web application to conduct business—and, of those, only 13 percent rely exclusively on the mobile app.

In some cases, the issue is poor implementation of technology. For instance, some providers incorporate optical character recognition (OCR) software in their apps to scan card receipts. These systems then attempt to match the receipts with transactions when they post. Unfortunately, there is sometimes a mismatch between receipts and transactions that requires manual resolution. In other cases, providers simply port their existing web application to their mobile app, failing to capitalize on the unique functionality and security that smartphones can offer.

Poor design is also significant factor in discouraging adoption. In part, this has to do with the procurement process. In large organizations, the needs of users are often translated into checklists of desired features. As a result, many commercial banks and other app vendors offer products that are feature-rich but hard to use.

Taking a fresh look at mobile design

An example of a more productive approach is one advocated by human-centered design pioneers such as IDEO, the Silicon Valley-based consulting firm. Rather than begin with assumptions about end-user needs and preferences, human-centered designers involve end users at every stage of the product management cycle. These designers rely on rapid, iterative development using low-resolution prototypes to test potential solutions with end users. They focus on users’ emotional responses to reveal functionality flaws and identify ease-of-use challenges. This approach often yields easy-to-use mobile apps designed with features and functionality that add real control and productivity improvements for commercial card customers.

Capital One’s survey clearly reveals that there is an appetite among payments professionals for mobile apps that have the easy functionality they associate with consumer products—but they are not enthusiastic about the offerings to date. The onus is on commercial card providers to work closely with end users to identify their needs and together develop solutions that truly address them in powerful and practical ways.