What is a good credit score?

Credit scores are three-digit numbers used to predict how likely a person is to pay their loans, credit card bills and other lines of credit on time. That’s simple enough. But trying to explain what a good score is can be more difficult.

If you’re looking for a quick answer, it’s probably best to start with credit-scoring companies FICO® and VantageScore®, which produce some of the most commonly used credit scores.

But there’s a lot more to it than that. Keep reading to take a closer look at credit scores, including how they’re determined, who’s looking at them and what you can do to monitor and improve yours.

Key takeaways

- Most people have more than one credit score, which vary based on how they’re calculated, when they’re calculated and what information is used to calculate them.

- FICO and VantageScore are two popular credit-scoring companies.

- Scores from FICO and VantageScore typically range from 300 to 850.

- FICO says good credit scores fall between 670 and 739.

- VantageScore says good scores fall between 661 and 780.

Good credit basics

According to the Consumer Financial Protection Bureau (CFPB), credit scores are based on information from your credit reports. And they’re calculated by credit-scoring companies like FICO and VantageScore using complex formulas called scoring models.

FICO considers anything between 670 and 739 a good credit score. And VantageScore says good credit scores fall between 661 and 780. Scores above those might be considered very good, excellent or exceptional.

Lenders, like credit card issuers or banks, ultimately determine for themselves what they consider a good credit score.

This video explains a little more about how credit works.

Why are there different credit scores?

Credit-scoring companies use different models to calculate credit scores. So what FICO and VantageScore consider to be good scores can vary. And models might weigh information in credit reports differently as part of their calculations. That’s why your scores may vary, even if just by a few points, when you compare them.

What’s considered good credit?

A good credit score depends on where a score comes from, who calculates it and who judges it. Lenders may set their own credit policies and standards to determine creditworthiness. That means that what FICO, VantageScore or anyone else considers good may not be the same.

Here are some general guidelines for how being within a score range can impact your choices:

- A poor to fair credit score could make it more difficult to qualify for many credit cards and loans. If you do qualify for an account, you may have to pay high fees and interest rates if you don’t pay your balance in full each month. You might need to start with a secured credit card or credit-builder loan to build your credit.

- A fair to good credit score may qualify you for more options, but you won’t necessarily receive the best rates or terms. You might find you can qualify for an unsecured credit card but have a harder time qualifying for a premium card.

- A good credit score could give you a better chance of qualifying for a card offering benefits like cash back and travel rewards. It may not have the best rates or terms though.

- A very good, excellent or exceptional credit score could qualify you for the best products with the lowest advertised rates. While creditors consider other factors when determining your eligibility and rates, your credit score likely won’t be what’s holding you back.

What’s a good FICO credit score range?

Established in 1989, Fair, Isaac and Company (FICO) helped standardize credit scoring. In the 30-plus years since, FICO has created multiple versions of its scoring models. But according to FICO, “the various FICO score versions all have a similar underlying foundation, and all versions effectively identify higher risk people from lower risk people.”

FICO classifies scores between 670 and 739 as good. Scores in that range are near or slightly above the U.S. average credit score. For this credit score range, FICO’s highest credit score is 850. In total, FICO breaks its scores into the following five categories:

Source: MyFICO.com

- Exceptional: 800-850

- Very good: 740-799

- Good: 670-739

- Fair: 580-669

- Poor: less than 580

FICO also has consumer credit scores tailored to different industries, such as auto and mortgage lending. These scores and scoring categories may vary from the scores above.

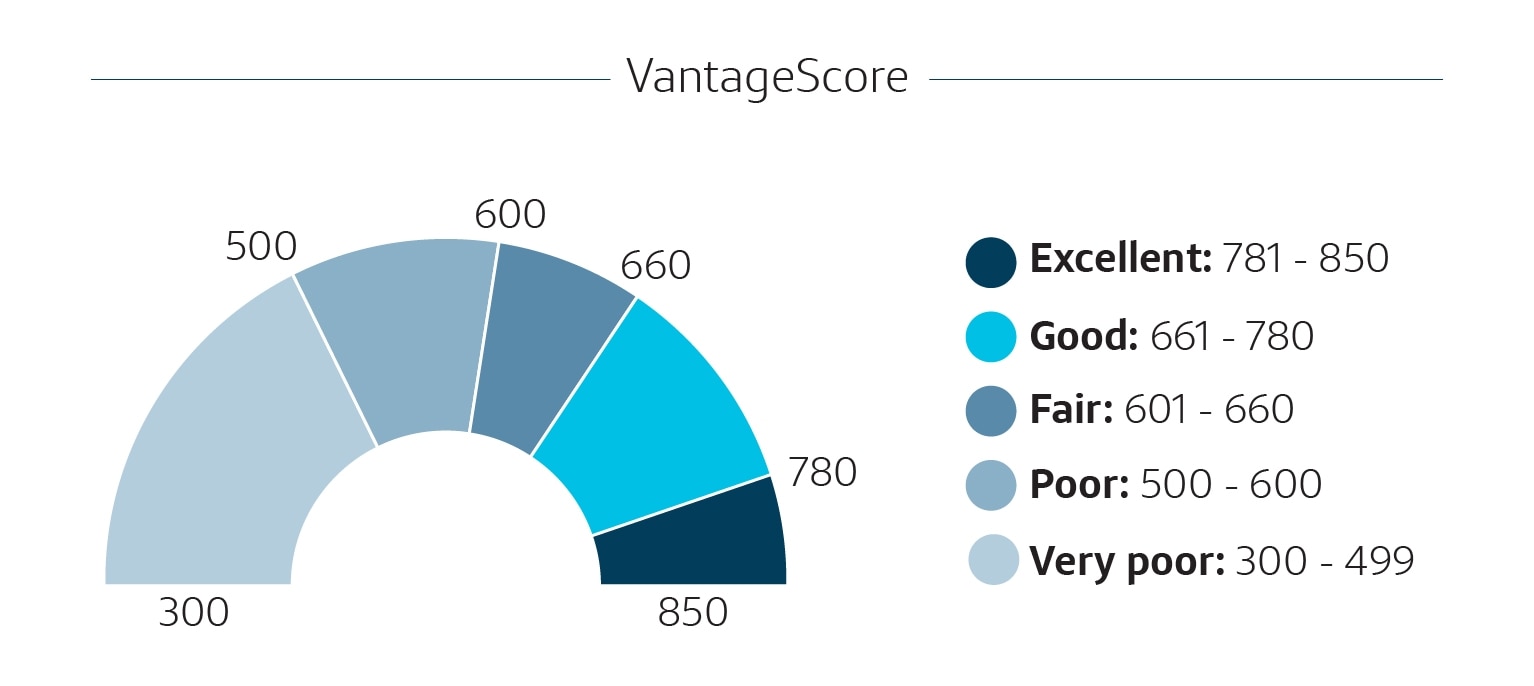

What’s a good VantageScore credit score range?

VantageScore entered the picture in 2006. It’s managed independently but was founded by the three major credit bureaus: Equifax®, Experian® and TransUnion®.

Credit card issuers and other lenders may rely on VantageScore credit scores in addition to FICO scores to judge loan or credit applications.

When it comes to VantageScore, scores between 661 and 780 are considered good. For VantageScore 3.0 and 4.0, the highest credit score is 850. VantageScore also breaks its scores into five groups but uses different credit ranges and category names than FICO:

Source: VantageScore.com

- Excellent: 781-850

- Good: 661-780

- Fair: 601-660

- Poor: 500-600

- Very poor: 300-499

Credit cards for good credit

Many credit card issuers offer cards for those with good credit scores. And Capital One is no different. So how does a credit card for good credit differ from one for excellent credit? It depends on the specific card, but rates and rewards might not be quite the same as a similar card for people with excellent credit. Cardholders with a Capital One credit card for good credit, for example, are not eligible for an early spend bonus or low intro APR.

Expand the sections below to get a look at how three of Capital One’s credit cards for good credit compare to similar cards for excellent credit.

What’s the difference between SavorOne Rewards for Good Credit and SavorOne Rewards?

SavorOne Rewards for Good Credit and SavorOne Rewards are two of Capital One’s dining and entertainment credit cards. Here’s how they compare.

|

SavorOne Rewards for Good Credit |

SavorOne Rewards |

|

|---|---|---|

| Credit score range | Good | Excellent |

| Rewards |

3% cash back on dining, entertainment, popular streaming services and grocery stores* 1% cash back on all other purchases 8% cash back at Capital One Entertainment5% cash back on hotels and rental cars booked through Capital One Travel |

3% cash back on dining, entertainment, popular streaming services and grocery stores* 1% cash back on all other purchases 8% cash back at Capital One Entertainment5% cash back on hotels and rental cars booked through Capital One Travel |

| Early spend bonus available | No | Yes |

| Low intro APR | No | Yes |

| Annual fee | No | No |

What’s the difference between Quicksilver Rewards for Good Credit and Quicksilver Rewards?

Quicksilver Rewards for Good Credit and Quicksilver Rewards are two of Capital One’s cash rewards credit cards. Here’s how they compare.

|

Quicksilver Rewards for Good Credit |

Quicksilver Rewards |

|

|---|---|---|

| Credit score range | Good | Excellent |

| Rewards |

1.5% cash back on every purchase, every day 5% cash back on hotels and rental cars booked through Capital One Travel |

1.5% cash back on every purchase, every day 5% cash back on hotels and rental cars booked through Capital One Travel |

| Early spend bonus available | No |

Yes |

| Low intro APR | No |

Yes |

| Annual fee | No | No |

What’s the difference between VentureOne Rewards for Good Credit and VentureOne Rewards?

VentureOne Rewards for Good Credit and VentureOne Rewards are two of Capital One’s travel rewards credit cards. Here’s how they compare.

|

VentureOne Rewards for Good Credit |

VentureOne Rewards |

|

|---|---|---|

| Credit score range | Good | Excellent |

| Rewards |

1.25X miles on every purchase 5X miles on hotels and rental cars booked through Capital One Travel |

1.25X miles on every purchase 5X miles on hotels and rental cars booked through Capital One Travel |

| Early spend bonus available | No | Yes |

| Low intro APR | No | Yes |

| Annual fee | No | No |

What affects your credit scores?

Credit-scoring models and credit reports are two big factors that determine your credit score. But if you don’t know what information from your credit report is being used, it’s not much help.

Here are a few factors the CFPB says make up a typical credit score:

- Payment history

- Debt

- Credit utilization rate

- Loans

- Credit age

- New credit applications

What factor has the biggest impact on a credit score?

FICO and VantageScore weigh factors differently. Here’s how FICO ranks them:

- Payment history: 35%

- Total debt: roughly 30%

- Length of credit history: roughly 15%

- Credit mix: roughly 10%

- New credit accounts: 10%

Here’s how different scoring factors are ranked in VantageScore 3.0 credit scores:

- Payment history: 40%

- Depth of credit: 21%

- Credit utilization: 20%

- Balances: 11%

- Recent credit: 5%

- Available credit: 3%

And here’s how they’re weighted in VantageScore’s latest credit-scoring model, VantageScore 4.0:

- Payment history: 41%

- Depth of credit: 20%

- Credit utilization: 20%

- Recent credit: 11%

- Balances: 6%

- Available credit: 2%

What doesn’t affect your credit scores?

Most credit-scoring models don’t consider certain information unless it’s part of your credit report. And even then, some parts of your credit report won’t impact your scores. Credit-scoring models generally don’t consider:

- Your age, race, nationality, color, sex, gender or marital status

- Where you live and work

- Your income, your job or whether you’re employed

- Whether you receive public assistance

- Political or religious affiliations

- The interest rates on your credit accounts

- Soft credit inquiries

Closed and paid-off accounts will stay on your credit reports and can continue to impact your scores until they fall off.

How to build a good credit score

Building good credit scores comes down to using credit responsibly over time. The same is true when it comes to maintaining a good credit score. Here are some things the CFPB says you can do:

- Pay your bills on time. Consider setting up automatic payments or electronic reminders to help you remember to make on-time payments.

- Stay below your credit limit. Experts recommend keeping your credit use below 30% of your available credit across all your credit card accounts.

- Apply only for the credit you need. If you apply for multiple credit cards and loans over a short period of time, credit card issuers and other lenders may think your financial situation has changed for the worse.

- Check your credit reports. Because your credit scores are based on the information in these reports, errors can hurt your credit scores.

How to monitor your credit score

Credit monitoring can help you detect fraud and track your credit scores.

One way to do this is by using a free credit tool like CreditWise from Capital One, which lets you access your TransUnion credit report and VantageScore 3.0 credit score. Using CreditWise won’t hurt your credit scores. And it’s free and available to everyone, even if you don’t have a Capital One account.

You can also learn how to get free copies of your credit reports by visiting AnnualCreditReport.com.

Good credit score FAQ

Here are some frequently asked questions about good credit scores:

How can you start building credit history?

There are types of credit designed to help customers who may be new to credit or are trying to rebuild their credit. Many people start with a secured credit card, student credit card, credit-builder loan or student loan. Even if you’re starting with bad credit, consistently using credit responsibly could help you build a good credit score.

What is a good credit score for buying a car?

There’s no specific credit score needed to buy a car. But auto loans will generally be more favorable when you have a credit score of 670 or higher, according to Experian. A good credit score can also result in better car loan terms. For instance, higher credit scores could help you get lower interest rates and a lower down payment.

What is a good credit score for buying a house?

Having a good credit score can also make it easier to buy a house and get better loan terms.

Conventional loans require a minimum credit score of 620, but a higher credit score could help you secure a lower interest rate, make a lower down payment and potentially save on private mortgage insurance.

Government-backed loans from the Federal Housing Administration or Department of Veterans Affairs may have modified credit guidelines, but good credit could still help get you the best possible terms.

Is it possible to improve your credit scores quickly?

Building good credit takes time, but there are steps you can take to help improve your credit scores. If you have a high credit utilization ratio that’s hurting your credit scores, paying down your revolving credit account balances might quickly improve your scores. Or if there’s incorrect negative information in your credit report, disputing the error and getting it corrected right away could help.

The CFPB also says to be wary of people or companies that say you can pay them to quickly fix your credit. If you need help managing credit, the U.S. Department of Justice has a list of approved credit counseling agencies you can refer to.

Good credit scores in a nutshell

Using credit accounts responsibly and paying your bills on time can help you establish credit and lead to good or even excellent credit scores. Having low credit card balances and avoiding late payments could also help you maintain good credit.

When it comes to credit cards you might qualify for with a good credit score, you may not get all the benefits of the most premium cards, but there are still good choices. You can find out which cards you might qualify for with pre-approval. It’s quick, only requires some basic info and won’t hurt your credit scores.

And remember, CreditWise offers an easy way to monitor your credit. It’s free and available to everyone, whether you’re a Capital One account holder or not. Using CreditWise won’t hurt your scores either.